Absorption Costing

Previous Lesson: Factory Overhead

Next Lesson: Product Costing Systems

In Absorption Costing, the product, services or activities are charged with a fair share of indirect cost. There are four-step process involved in charging overhead cost to product or services:

- Overhead Allocation,

- Overhead Apportionment,

- Overhead Re-Apportionment and,

- Overhead absorption Rate also called Overhead Recovery.

Overhead Allocation

Overhead allocation is first of the three stages in establishing a full cost for a product or services. Overhead allocation is the process of charging a whole item of cost to a cost centre. Cost Centre is defined as to a unit or organization for which costs are accumulated or computed. In other words, cost centre is area, machine, or person to whom direct and indirect costs are allocated. Factory overhead costs are incurred in three main centers:

- Production centers costs arising in production departments such as the costs of fuel, indirect material, depreciation and supervision

- Service centers the cost of operating support departments or sections within the factory, for example, the costs of materials handling, production control etc.

- General costs centers general production overhead such as factory rent/taxes, heating and lighting and canteen

An item of expenses which can be directly related to a cost centre is to be allocation to the cost centre. For example , depreciation of a particular machine should be allocated to a particular cost centre if the machine is directly attached to the cost centre. When factory overhead expenses are not identified with a specific product, they are charged to product by a process of overhead allocation. Allocations may be made for each item of expense incurred and the allocations made at the end of the accounting period. The purpose of cost accounting is to provide information to the management. Management need to know cost per unit as a basis for decision making.

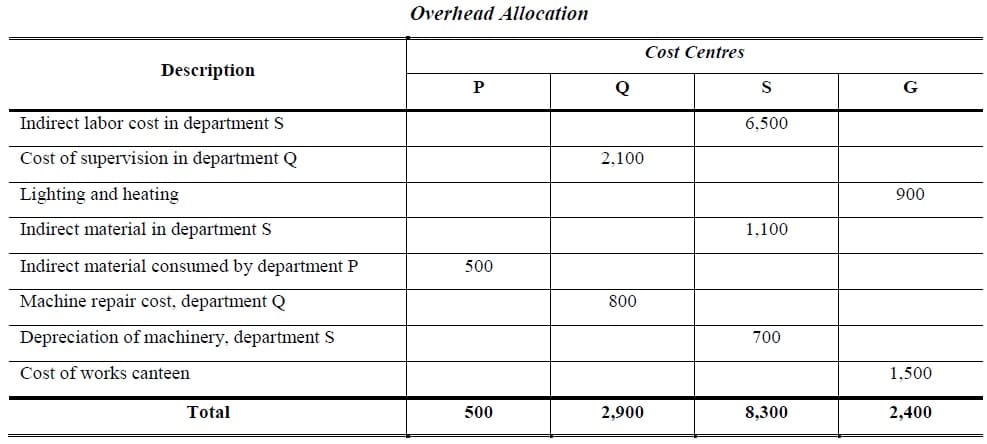

Example 1:

A manufacturing business operates with two production departments P and Q and a department S. It manufactures soup and shampoo. It incurs the following costs in a given period.

Indirect labor cost in department S Rs. 6,500

Direct labor cost in department P 4,700

Cost of supervision in department Q 2,100

Direct material cost in department P 10,300

Lighting and heating 900

Machine repair cost, department Q 800

Indirect material in department S 1,100

Depreciation of machinery, department S 700

Indirect material consumed by department P 500

Cost of works canteen 1,500

Requirement: Allocate these costs as overhead cost to the following cost centres:

Production Cost Centre (P), Production Cost Centre (Q), Service Cost Centre (S) and General Cost Centre (G)

Solution:

>> Practice Multiple-choice Questions: Product Costing Systems MCCQ

Overhead Apportionment

Once overhead costs have been allocated to cost centers, general overhead must be shared out or apportioned. This may be to production or services cost centers. Overhead apportionment is the process of sharing out overhead costs on fair basis. Overheads are to be apportionment to different cost centers based on following two principle. Cause and Effect: Cause is the process or operation or activity and effect is the incurrence of cost. Benefits received: Overheads are to be apportioned to the various cost centres in proportion to the benefits received by them

Example 2:

A general cost in a manufacturing company is factory rental. Annual rental costs are Rs. 80,000. How this cost should be apportioned between production cost centres and services cost centres? Rental costs are usually apportioned between cost centres on the basis of the floor space taken up by each centre. Suppose that three cost centres have floor space of 50,000 square meters; Production cost centre (A) has 10,000 square meters, Production cost centre (B) has 15,000 square meters and Service cost centre (C) has 25,000 square meters.

Solution:

Production Cost Centre (A) = 80,000 * 10,000 / 50,000 = Rs. 16,000

Production Cost Centre (B) = 80,000 * 15,000 / 50,000 = Rs. 24,000

Service Cost Centre (C) = 80,000 * 25,000 / 50,000 = Rs. 40,000

>> Further Practice: Process Costing Problems and Solutions.

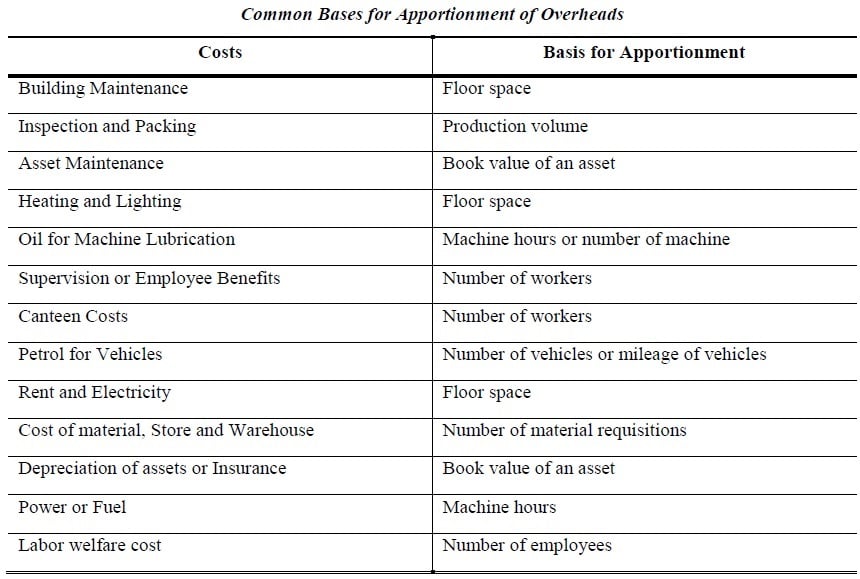

Bases for Overhead Apportionment

- Basis of apportionment must be rational to distribute overheads

- Once the base is selected the same is to be followed consistently

- However, change in basis for apportionment can be adopted only when it is considered necessary due to change in circumstances like change in technology, degree of mechanization product mix etc.

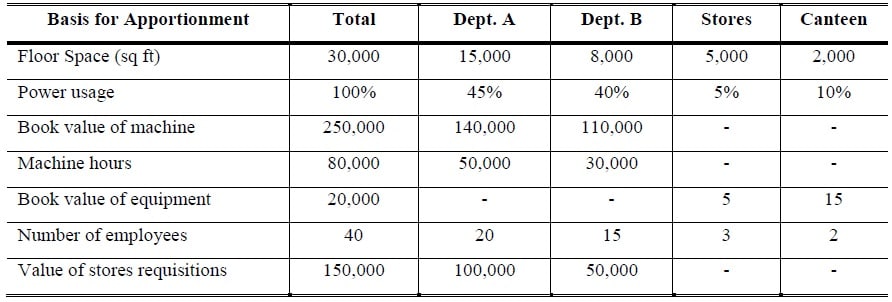

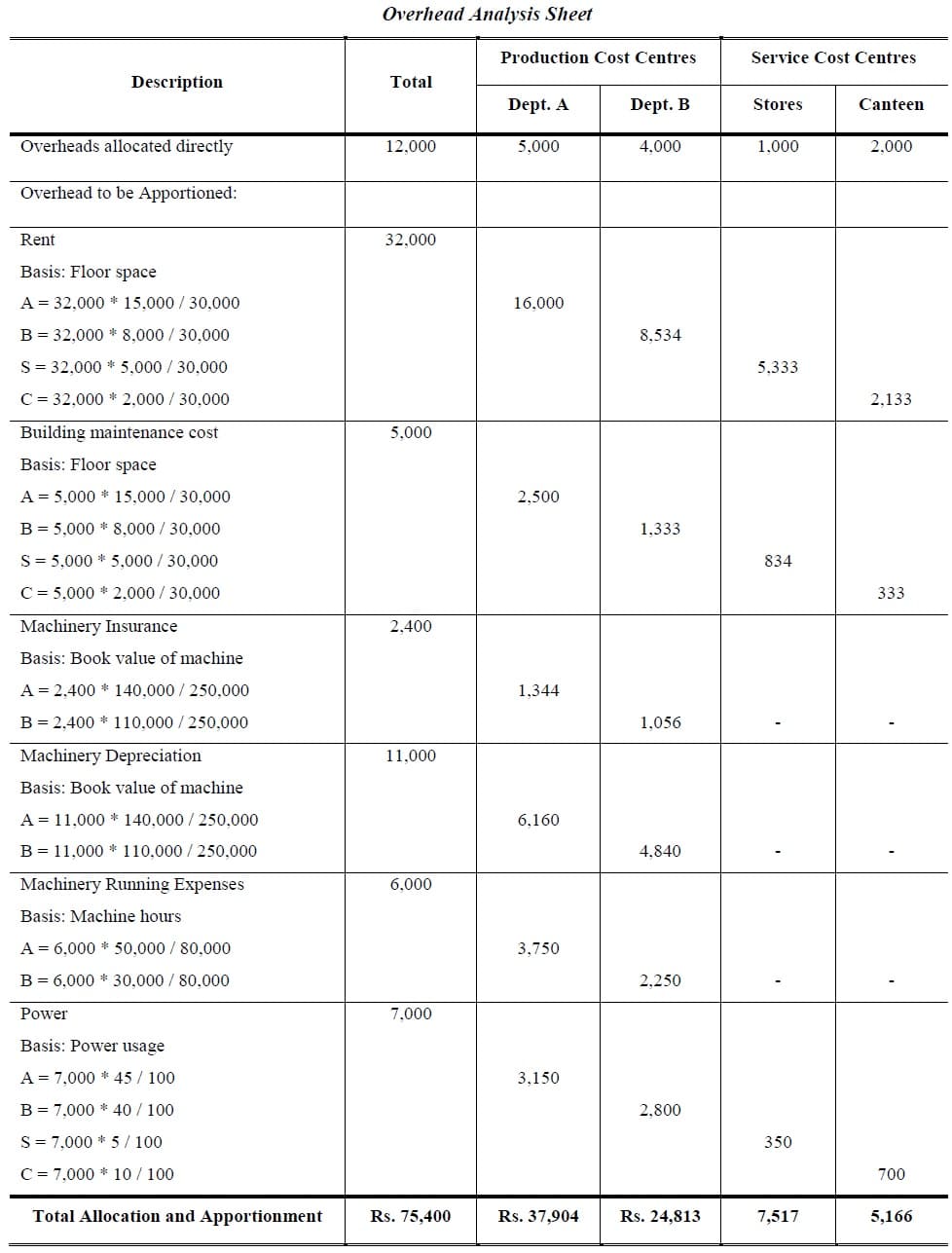

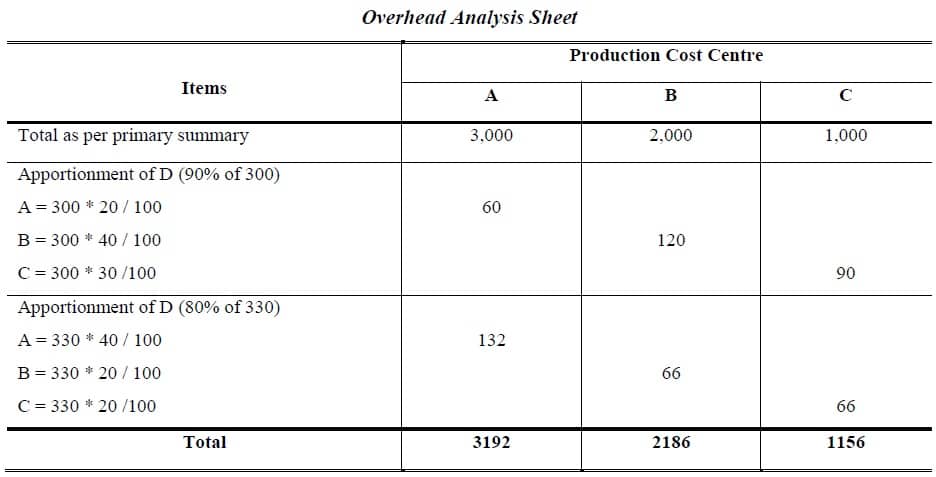

Example 3:

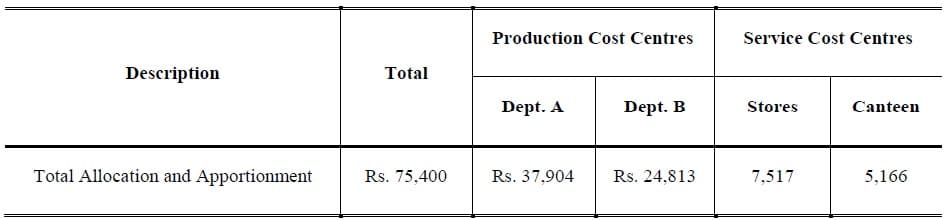

An organization has two production department A and B and two services departments, Stores and canteen. The general overhead costs for the organization in total are as follows:

Rent Rs. 32,000

Building maintenance costs 5,000

Machinery insurance 2,400

Machinery depreciation 11,000

Machinery running expenses 6,000

Power 7,000

There are also specific costs that have already been allocated to each cost centre as follows:

Department A Rs. 5,000

Department B 4,000

Stores 1,000

Canteen 2,000

The following information about the various cost centers is also available:

Required: Allocate and apportioned the cost to the four departments by making Overhead Analysis Sheet?

Solution:

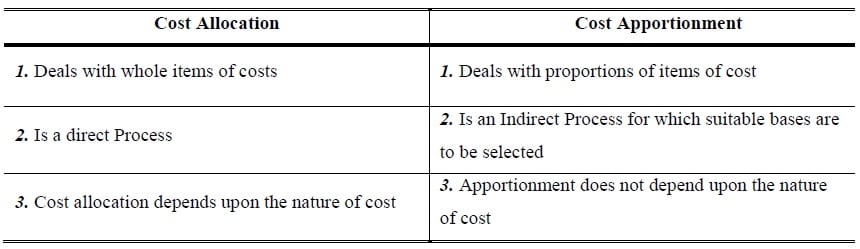

Difference between Cost Allocation and Cost Apportionment

>> Practice Multiple-choice Questions: Product Costing Systems MCCQ

Re-Apportionment

Organizations may have service departments (canteen, maintenance and administration) which cannot be related to any income producing activity. To find the full cost of a cost unit these department costs should also be absorbed into the unit cost. Therefore, service departments must be apportioned to the various departments producing the products or services. There are three methods are used for re-apportionment:

- Direct Distribution Method

- Step-Down Method

- Algebraic Distribution Method

Direct Distribution Method

- In this method services cost centres will be re-apportioned to production cost centre only

- In this situation where service cost centres do not service each other (Non-Reciprocal Apportionment)

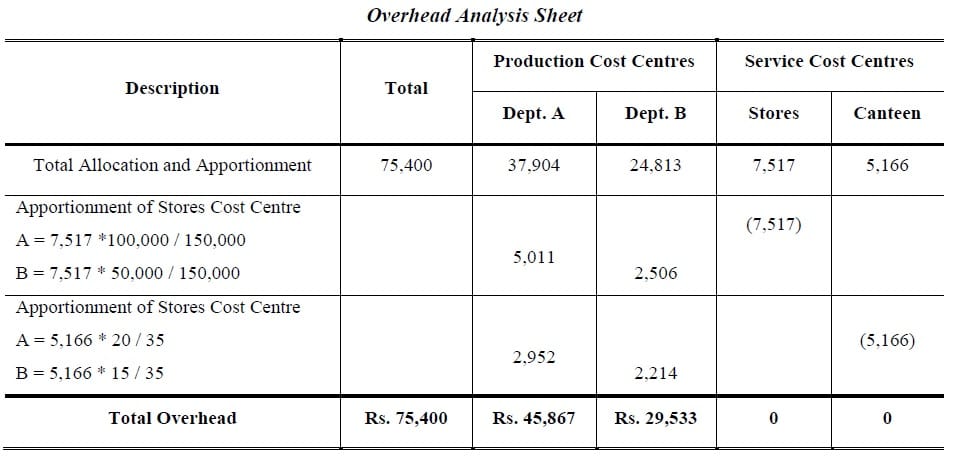

Example 4:

Using the information produced in the previous example, the allocated and apportioned overhead costs are:

The apportionment of the stores cost centre will be on the basis of the value of requisitions by each production cost center. The apportionment of the canteen costs should be on the basis of the number of employees in production dept. A and B:

Requirement: Show how the service cost centre costs should be re-apportioned and the resulting total overhead costs of each production cost centre assuming that store cost centre does not work for canteen and canteen does not work for store cost centre?

Solution:

>> Practice Multiple-choice Questions: Product Costing Systems MCCQ

Step-Down Method

Some organizations use the step-down method, also called the sequential or repeated allocation method. Which allocates services-department costs to other services departments and to production departments in a sequential manner that partially recognizes the mutual services provided among all service depts. (Reciprocal pportionment). Distributes service department costs regressively to other service departments and then to production departments.

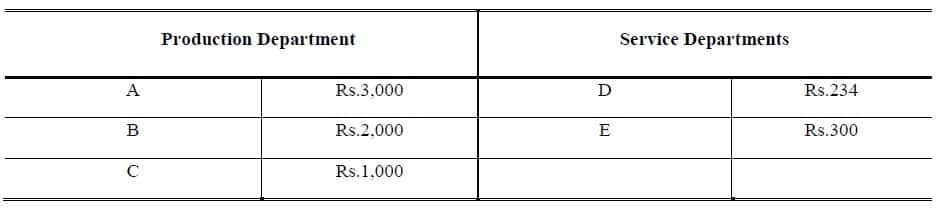

Example 5:

A company has three production departments and two service departments. Distribution summary of overheads is as follows:

The expenses of service departments are charged on a percentage basis which is as follows:

Requirement: Find out the total overheads of production departments by step-down method?

Solution:

>> More Questions and Solutions: Economic Order Quantity Problems and Solutions

Algebraic Distribution Method

It is also reciprocal apportionment using equation. Distributes costs by simultaneous equations recognizing the relationship of services rendered by departments to each other.

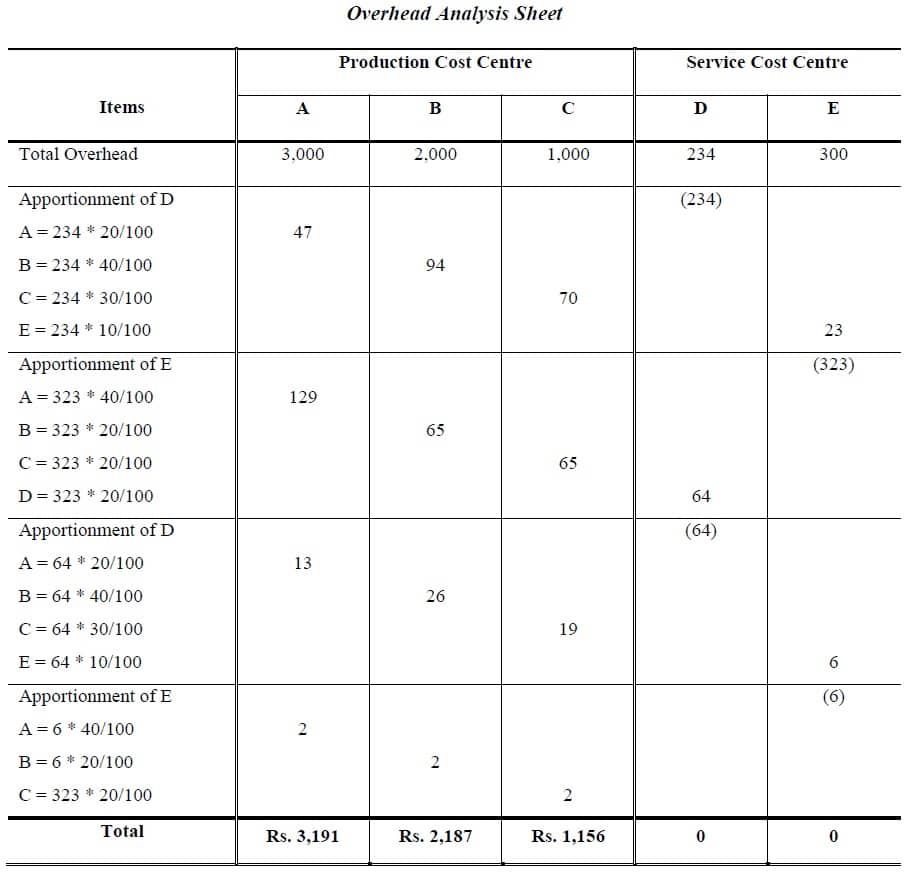

Example 6:

A company has three production departments and two service departments. Distribution summary of overheads is as follows:

The expenses of service departments are charged on a percentage basis which is as follows:

Requirement: Find out the total overheads of production departments by Algebraic Distribution Method?

Solution:

Let x denotes total overhead of service department D

y denotes total overhead of service department E

Therefore, x = 234 + 0.2y……………… (1)

y = 300 + 0.1x ……………… (2)

Re-arrange the equation

x – 0.2y = 234…………..…… (3)

– 0.1x + y = 300…………….…. (4)

To solve the equations multiply by 10 to remove decimals

10x – 2y = 2,340……………….. (5)

– x + 10y = 3,000………..…..….. (6)

Multiplying (6) equation by 10 and solving

10x – 2y = 2,340

-10x + 100y = 30,000

98y = 32,340

y= 32,340 / 98

y = 330

Putting the value of y in equation (1)

x = 234 + 0.2y……………… (1)

x = 234 + 0.2 (330)

x = 300

>> Practice Multiple-choice Questions: Product Costing Systems MCCQ

Overhead absorption Rate

An absorption rate is the rate at which overheads are added to costs. Production overhead costs are absorbed into product costs on a particular bases selected by the organization. The calculation of an overhead absorption rate requires two elements i.e. the total overhead attributable to a cost center and the absorption base. The absorption bases should be appropriate. The most common bases of absorption are:

- Percentage of direct material cost

- Percentage of direct labor cost

- Percentage of prime cost

- Rate per unit produced

- Rate per labor hour

- Rate per machine hour

Overhead absorption RateFormula

Once an Overhead absorption rate has been calculated, the amount of overhead absorption can be calculated as follow:

Overhead absorption = Actual Activity Level * Overhead Absorption Rate

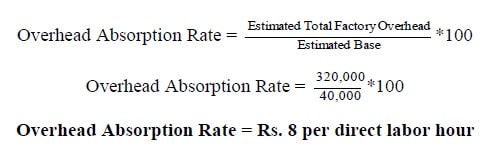

Example 7:

The Company estimated that it would incur Rs. 320,000 in manufacturing overhead costs and would work 40,000 direct labor-hours. What is the company’s Overhead Absorption rate?

Solution:

>> Practice Multiple-choice Questions: Product Costing Systems MCCQ

Product and Period Costs

- All manufacturing costs are product costs i.e. direct material, direct labor and factory overhead costs

- Period costs are not associated with the production of goods. Some examples of period costs are:

- Selling, advertising, marketing costs

- Delivery of products to customers (e.g., freight-out, transportation-out, delivery expense)

- General and administrative costs

- Corporate occupancy such as corporate rent, corporate insurance, corporate utilities, corporate depreciation

>> Practice Multiple-choice Questions: Product Costing Systems MCCQ

Related Topics

Factory Overhead Problems

References

Mukharji, A., & Hanif, M. (2003). Financial Accounting (Vol. 1). New Delhi: Tata McGraw-Hill Publishing Co.

Narayanswami, R. (2008). Financial Accounting: A Managerial Perspective. (3rd, Ed.) New Delhi: Prentice Hall of India.

Ramchandran, N., & Kakani, R. K. (2007). Financial Accounting for Management. (2nd, Ed.) New Delhi: Tata McGraw Hill.

Appreciate one additional write-up. Exactly where else could anyone have that sort of details on this kind of a ideal way with words? Ive got a presentation subsequent week, and Im towards the search for this sort of knowledge.

Nice post on cost accounting.

I am no longer positive where you are getting your information, however good topic. I needs to spend some time studying much more or working out more. Thank you for magnificent information I was searching for this information for my mission.

I think this is among the most important information for me. And i’m glad reading your article. But want to remark on some general things, The web site style is perfect, the articles is really great : D. Good job, cheers

Please send me new post by mail