Classified Balance Sheet

Previous Lesson: Balance Sheet

Next Lesson: Fund Flow Statement

Classified Balance Sheet is often use by companies to improve users’ understanding of a company’s financial position. Financial Statements of the company show its financial health, position and its operational activities. Balance Sheet is a principal financial statement which shows the financial standing of the company at a particular time. It presents the snapshot of the company’s position at the date it is prepared. Other titles of balance sheet include statement of financial position and statement of financial condition. Classified balance sheet is used to provide picture to insiders and outsider about the financial health of organization in classified manners. This statement breaks down all accounts into smaller categories to create a more meaningful and useful financial report (Weygandt, Kimmel, & Kieso, 2012).

The most common classifications used within a classified balance sheet are:

- Current Assets

- Long Term Investments

- Property, Plant and Equipment (PP&E)

- Intangible Assets

- Current Liabilities

- Long Term Liabilities

- Shareholders’ Equity

Classified Balance Sheet Format

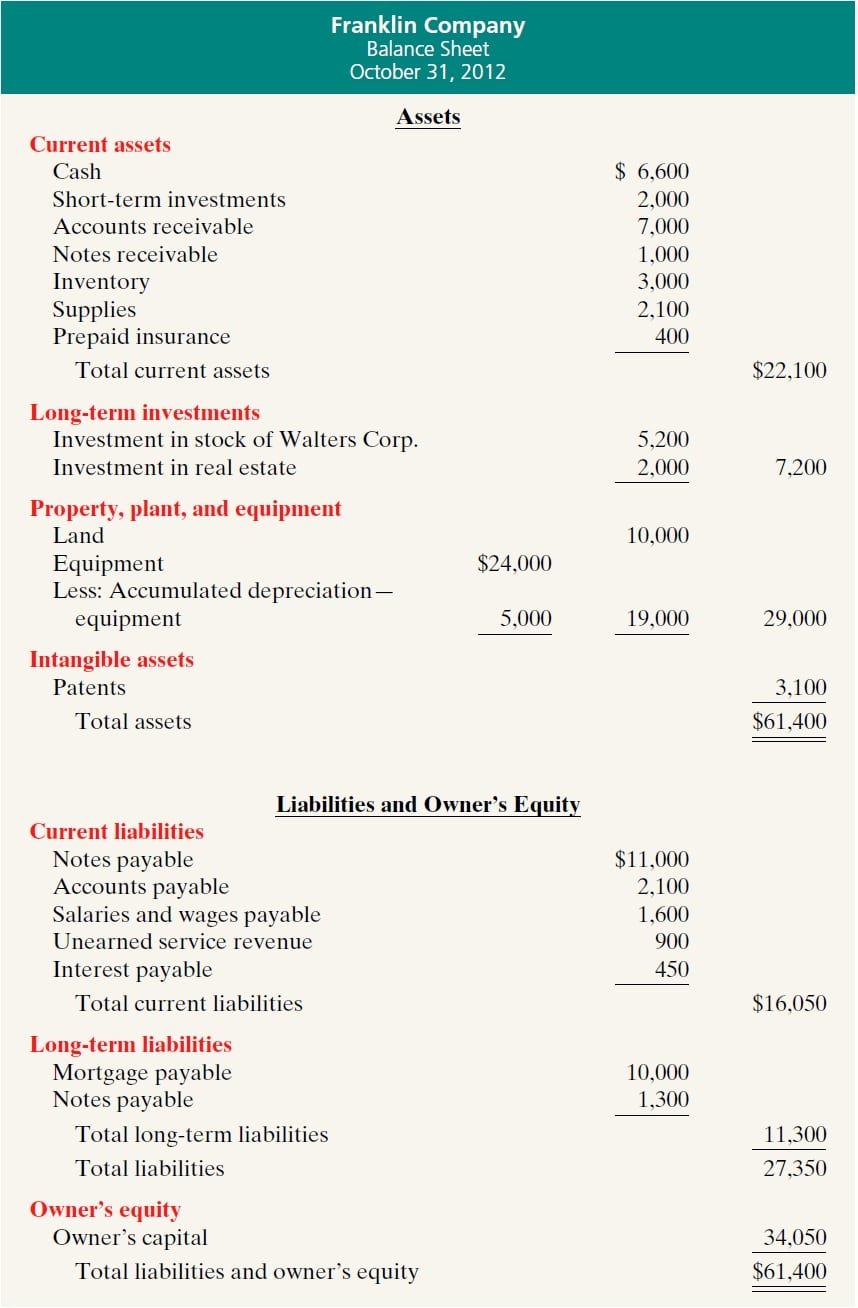

In Classified Balance Sheet Format, there are three basic elements of like Assets, Liabilities and shareholder equity. Information regarding their details can either be provided by wider categories or it can be presented by subcategories to show classification of its basic elements. In classified balance sheet accounts of assets are sub-categorize as current asset, long-term investments, property, plant & equipment and intangible assets, on the other hand liabilities as current liabilities and long-term liabilities on basis of their maturity along with owner’s or shareholders’ equity.

(Source: Weygandt, Kimmel, & Kieso, 2012)

Accounts of Classified Balance Sheet

A classified balance sheet contains following sections:

Current Assets:

Current assets are liquid as they can be converted into immediately as compared to fixed assets which are not highly liquid. Currents assets are further listed under this category on basis of liquidity such that most liquid item is at top of list and rest are listed from most liquid to least liquid. Category of current assets include cash and equivalent, account receivable, inventories, prepaid expenses, and other short term nature assets.

Long Term Investments:

Long term investments are assets which can be converted in to cash after a year. It usually non-current investment made by business. For example investment in another company by means of stock or bonds or investment in real estate.

Property, Plant & Equipment:

This class of asset is comparatively fixed in nature. Which include property, plant, machine, equipment, building etc.

Intangible Assets:

Assets which couldn’t see or touch is called intangible assets like patents, goodwill, rights etc.

Current Liabilities:

Current liabilities are items with shortest maturity period. This include note payable, account payable, accrued expense, current portion of installment, deferred income tax and long term includes bond payable, bank loans etc.

Long Term Liabilities:

Those obligation which will be payable after a year is called long term liabilities. For example bank loan, mortgage loan etc.

Shareholder’s Equity or Owner’s Equity:

The shareholder equity is categorized into preferred stock, common stock, capital in excess of par and retained earnings. Whereas in unclassified balance sheet different accounts of assets, liabilities and shareholder equity are presented as a list on the same criteria as used by classified balance sheet but without classifying the accounts in subcategories like Current assets, fixed assets and intangible assets etc.

Advantage of Classified Balance Sheet

Classified balance sheet enables the user either insider or outsider to access the data with ease as all information is sorted out in categories. It makes clear distinction between the groups which enable the company to easily identify its composition of total assets and their financing. It facilities the company to easily identify and makes any potential changes or make a decision regarding investing in current or fixed assets and deciding the source and mix of financing. Moreover, it enables the users to easily calculate ratios for financial statement analysis that uses items of balance sheet for calculating ratios like acid test ratios.

References

Weygandt, J. J., Kimmel, P. D., & Kieso, D. E. (2012). Accounting Principles (10th ed.). Hoboken: John Wiley & Sons, Inc.

Mukharji, A., & Hanif, M. (2003). Financial Accounting (Vol. 1). New Delhi: Tata McGraw-Hill Publishing Co.

Narayanswami, R. (2008). Financial Accounting: A Managerial Perspective. (3rd, Ed.) New Delhi: Prentice Hall of India.

Ramchandran, N., & Kakani, R. K. (2007). Financial Accounting for Management. (2nd, Ed.) New Delhi: Tata McGraw Hill.

What is the difference between a balance sheet and a classified balance sheet?