Bill of Exchange

Previous Lesson: Company Final Accounts

Next Lesson: Partnership

Bill of exchange as “an instrument in writing containing an unconditional order, signed by the maker, directing a certain person to pay a certain sum of money only to or to order of, a certain person or to the bearer of the instrument”. In order that an instrument may be called a bill of exchange it should satisfy the following conditions

- It must be in writing

- It must contain an unconditional order to pay

- It must be signed by the drawer

- The order must be to pay a certain sum of money

- There must be three parties to the instrument

Following are three parties:

- Drawer: It is the person who is the maker of the bill of exchange. It is the person who has sold the goods and for receiving the payment from the debtor he draws a bill of exchange

- Drawee or Acceptor: It is the person on whom the bill of exchange is drawn and he has to make the payment to the supplier of goods

- Payee: It is the person to whom the payment has to be made. It may be the drawer himself if he has not discounted the bill with any third party

In calculating the due date of payment it is customary in business to allow three additional days to the drawee or acceptor to meet the bill. The extra days are called “days of grace” or “grace days”. Thus a bill dated 15th March, for three months becomes payable on the 18th June and this is the due date.

>>> Practice Bill of Exchange MCQs

1. Recording Transactions

For the purpose of accounting, bills are classified under two heads:

- Bills receivable

- Bills payable

1.1 Bills Receivable

A bill of exchange is treated as a bill receivable by one who is entitled to receive the sum due on it. When we draw a bill or receive it by endorsement from our debtors, it is our bill receivable (B/R) and on maturity of such bill if it is held up to that time, we shall receive specified amount from the acceptor.

1.2 Bills Payable

A bills payable is regarded as bill payable by one who has to pay it on the due date. When we accept a bill and thereby become liable to pay on its maturity, it is our bill payable (B/P). It means the same bill is a bill receivable to one party and a bill payable to the other.

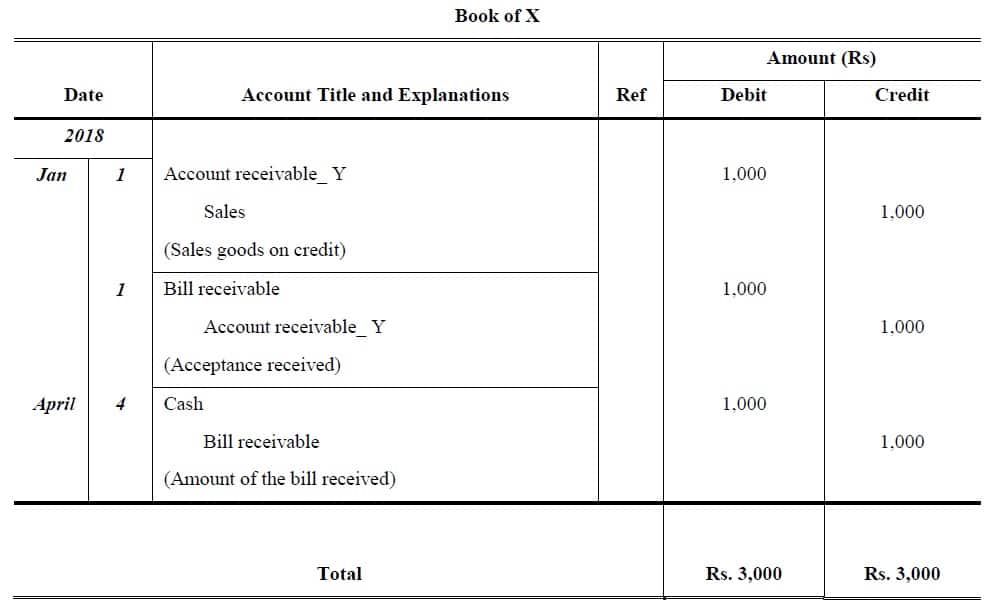

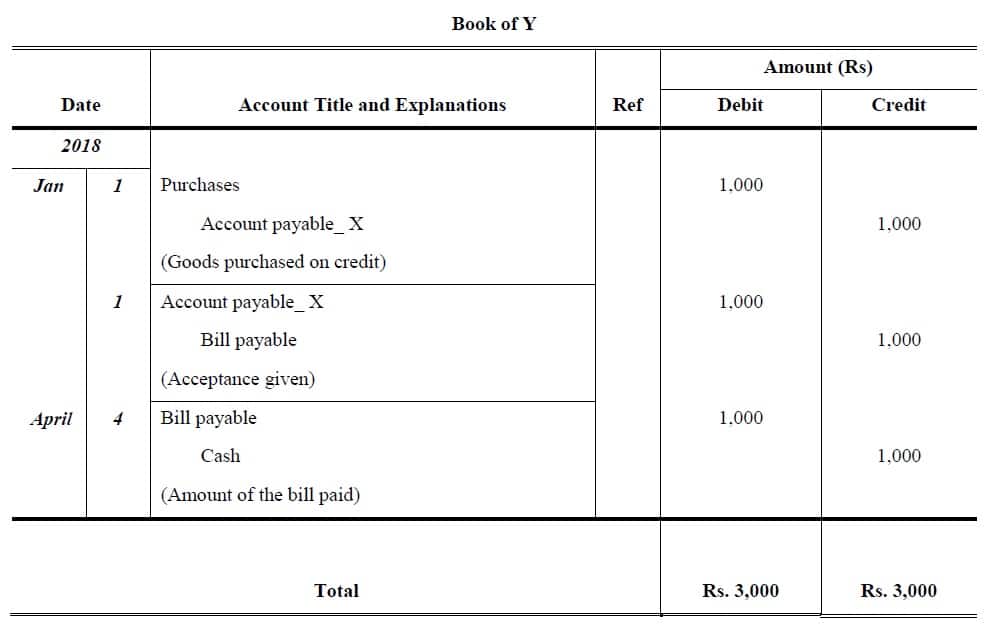

Example 1:

X sold goods to Y for Rs. 1,000 on 1st January 2018 and draws on Y a bill of exchange at three months for this amount. Y accepts the bill and returns it to X. The bill is dully met at maturity. Show the journal entries to record the transactions in both the parties’ books.

Solution:

2. Discounting of Bills

- If the holder of a bill is need of money before the due date of the bill he may sell it to the bank

- One of the most frequent means of short-term funding is the discount of bills of exchange

- The Bank carries out discounting bills of exchange issued by its customers or by other banks, with a discount rate established with decision by the Bank’s management

- This immediately pays out the amount of the bill reduced by discounting costs

- The bill of exchange is sent on collection at the maturity date

- The acceptor has no concern with the discounting of the bill. He has to pay it on the due date to the holder, therefore, there will be no journal entry for discounting of the bill of exchange

>>> Practice Bill of Exchange Quiz 1

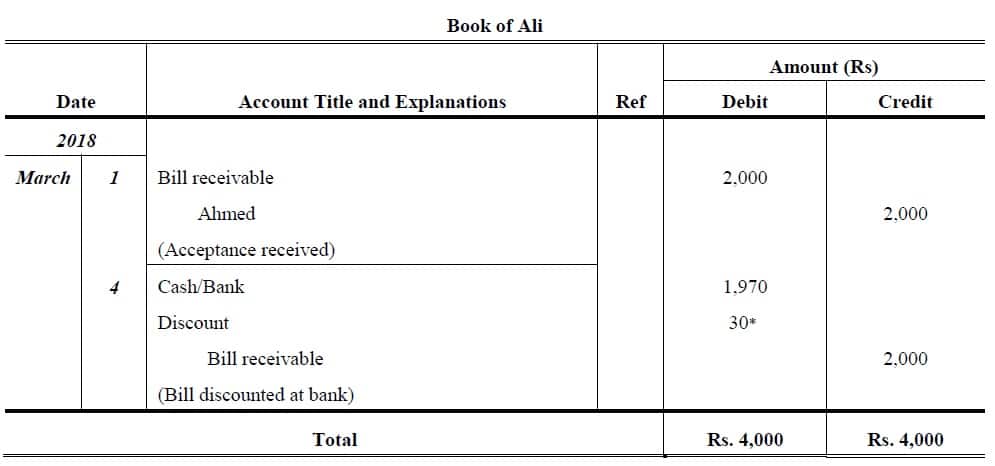

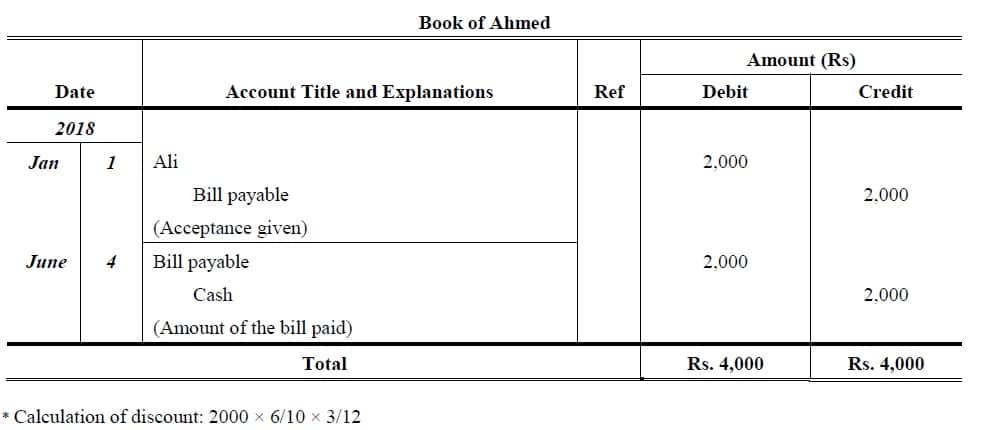

Example 2:

Mr. Ali draws a three month bill for Rs. 2,000 on Mr. Ahmed on the 1st March, 2018 for the value received. Ahmed accepts it and returns it to Ali, who discounts it on 4th March, 2018 with his bank at 6 per cent per annum. Ahmed pays acceptance on the due date.

Solution:

3. Endorsement of Bill of Exchange

Sometimes the drawer of the bill does not keep the bill with him until the date of the maturity. He endorses it to some other party in payment of the debt due from him. When a bill of exchange is negotiated i.e., transferred from one person to another person, each person through whose hands it passes, must write his name on the back of the bill.

>>> Practice Bill of Exchange Quiz 2

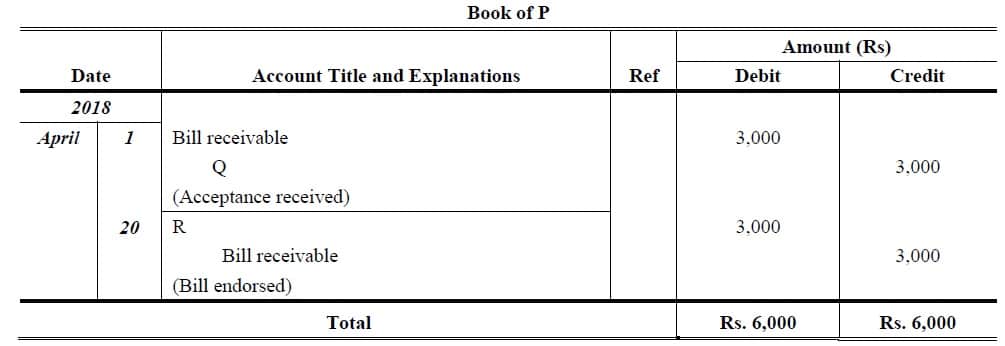

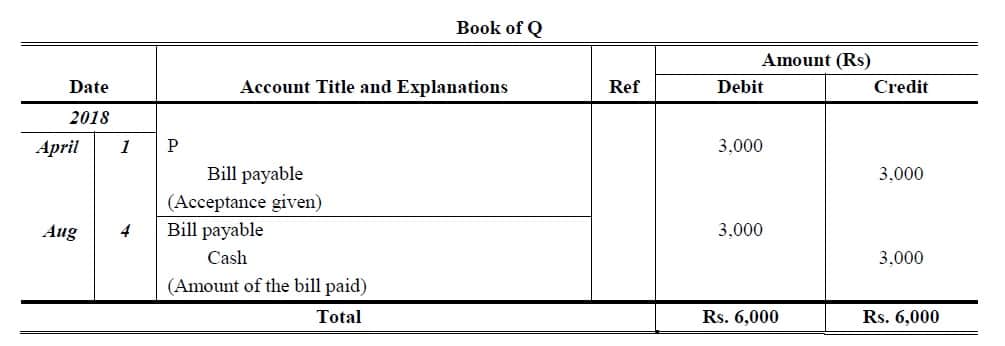

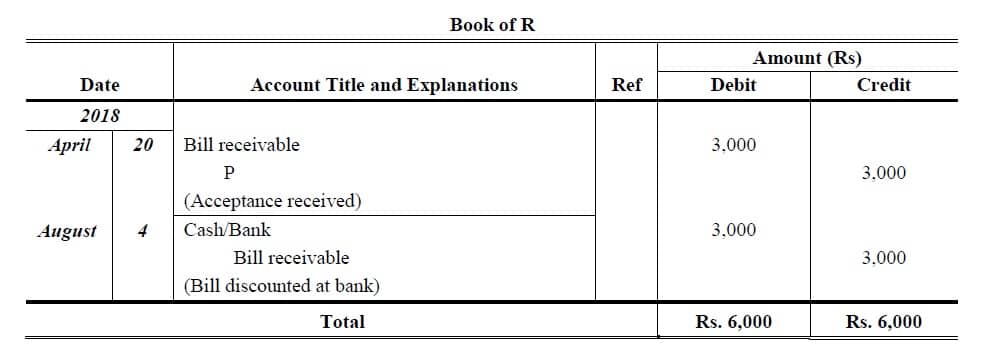

Example 3:

A bill for Rs. 3,000 is drawn by P on Q on April 1st, 2018 and accepted for 4 month. P transfers it to his creditor R on 20th April 2018. On the due date the acceptance is duly met. Record the above transactions in the books of P, Q and R.

Solution:

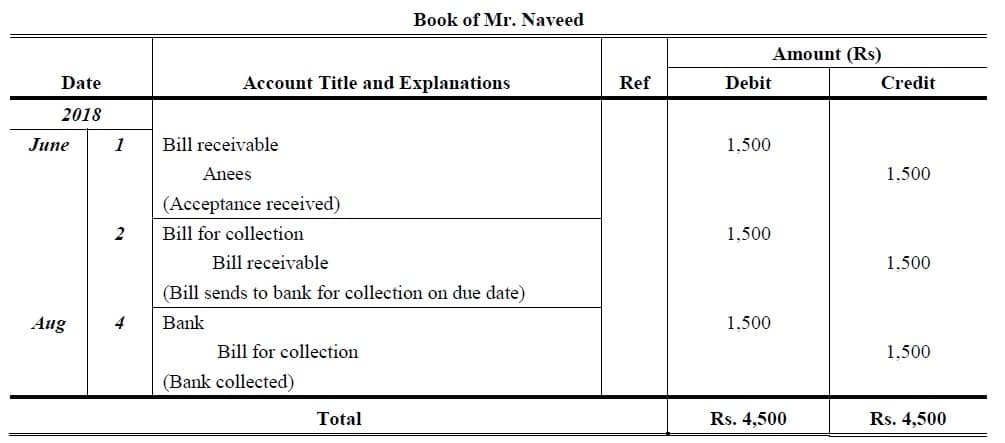

4. Sends the Bill to the Bank for Collection

Bills sent to other banks for collection should be endorsed in their favor as agents for collection.

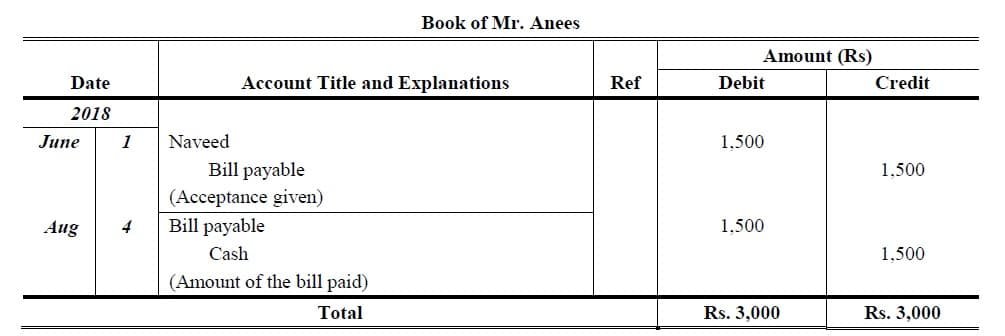

Example 4:

A bill for Rs. 1,500 is drawn by Mr. Naveed on Mr. Anees on June 1st, 2018 and accepted for 2 month. Mr. Naveed sends the bill to the bank for collection on 2nd June 2018. On the due date the acceptance is duly met. Record the above transactions in the books of Mr. Naveed and Mr. Anees.

Solution:

5. Dishonor of a Bill of Exchange

A bill of exchange is said to be dishonored when the drawee refuses to accept or make payment on the bill. A bill may be dishonored by non-acceptance or non-payment. If the drawee refuses to accept the bill when it is presented before him for acceptance, it is called dishonor by non-acceptance. If the drawer has accepted the bill, but on the due date, he refuses to make payment of the bill, it is called dishonor by non-payment.

Reasons for Dishonor of Bill

| Situation | In the Book of A | In the Book of B |

| (1) When A retains the bill till to maturity and dishonored | B | Bill Payable |

| Bill Receivable | A | |

| (Being Bill dishonored at maturity) | (Being Bill dishonored at maturity) | |

| (2) When A discounts the Bill with the banker and dishonored | B | Bill Payable |

| Bank | A | |

| (Being the bill previously discounted now dishonored). Bill: Bank Account will be credited by the full value of bill. | (Being Bill dishonored at maturity) | |

| (3) When A endorsed the bill in favor of C and dishonored | B | Bill Payable |

| C | A | |

| (Being the bill previously endorsed, now dishonored) | (Being Bill dishonored at maturity) | |

| (4) When A sends the Bill to banker for collection and dishonored | B | Bill Payable |

| Bill for Collection | A | |

| (Being the bill previously sent for collection, now dishonored) | (Being Bill dishonored at maturity) |

(Bill: Assuming that A is Drawer and B is Drawee)

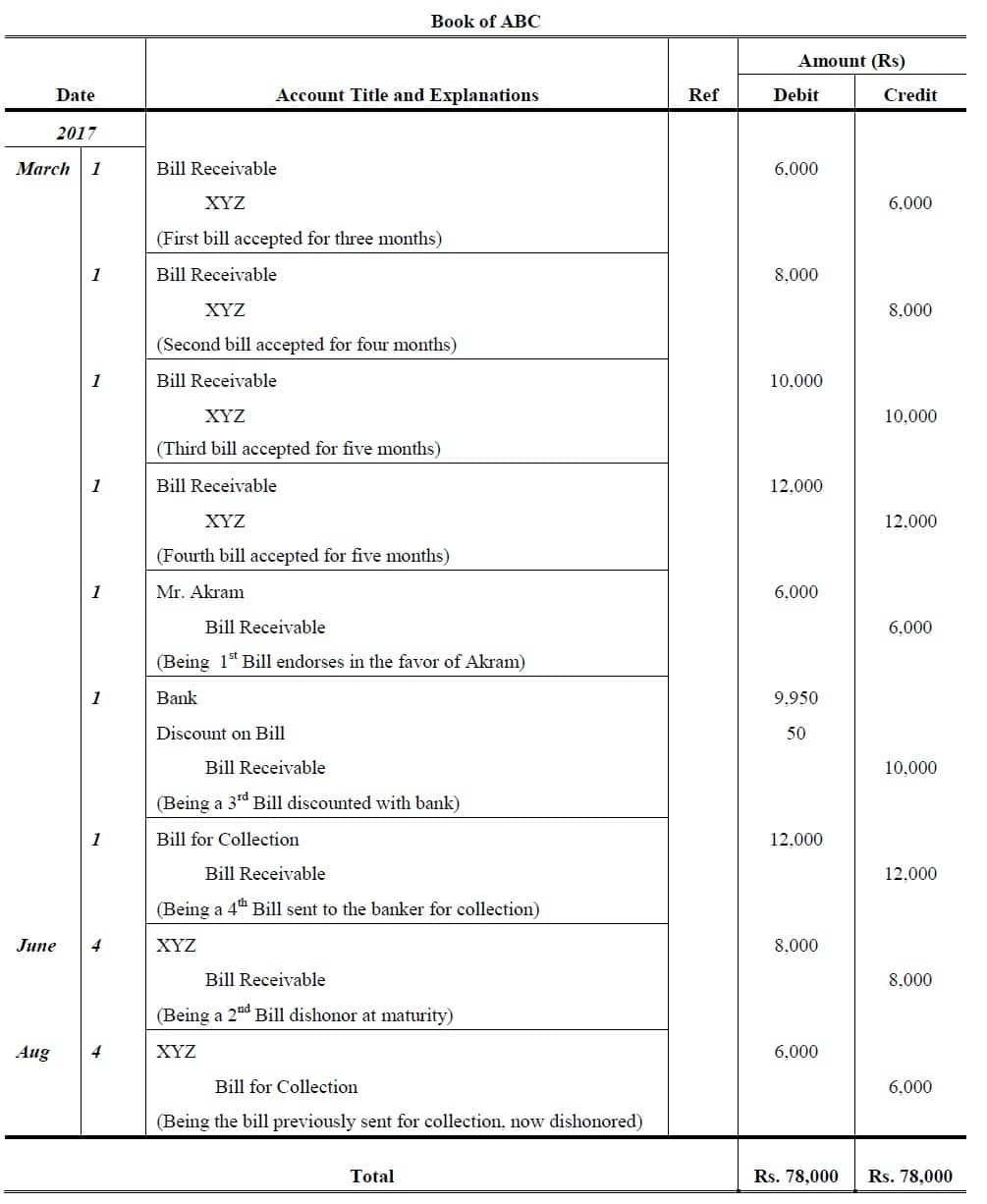

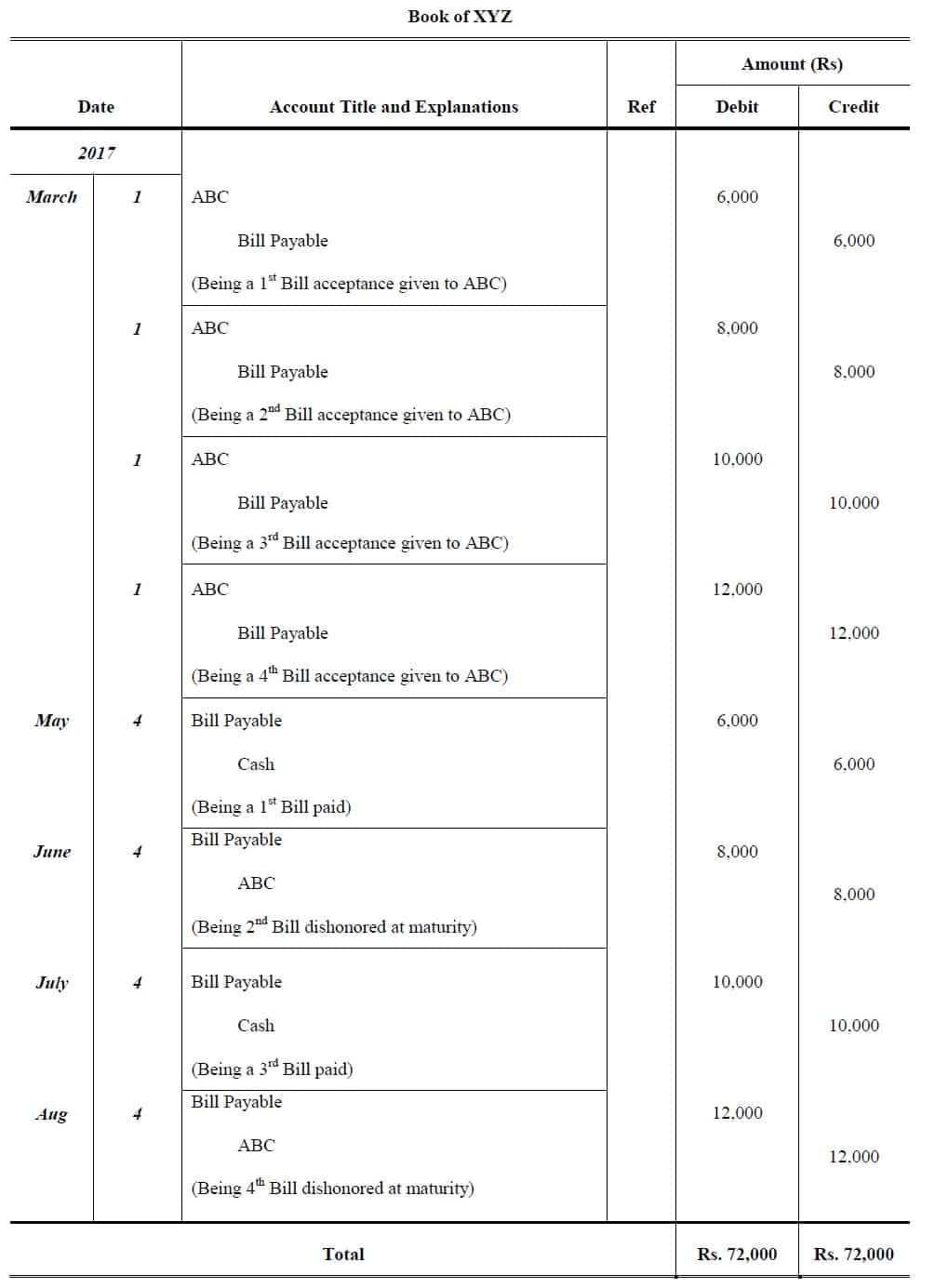

Example 5:

On March 1st, 2017 ABC Company received four accepted bills for XYZ Company of worth Rs. 6,000, Rs. 8,000, Rs. 10,000 and 12,000 for two, three, four and five month respectively. The first Bill of worth Rs. 6,000 endorsed to Mr. Akram; the second bill of worth Rs. 8,000 held till maturity; third bill of Rs. 10,000 was discounted for Rs. 50 discount on Bill and last Bill of Rs. 12,000 sent to bank for collection. At maturity First and third bill honored and second and fourth Bill dishonored.

Pass Journal entries in the book of ABC Company and XYZ Company.

Solution:

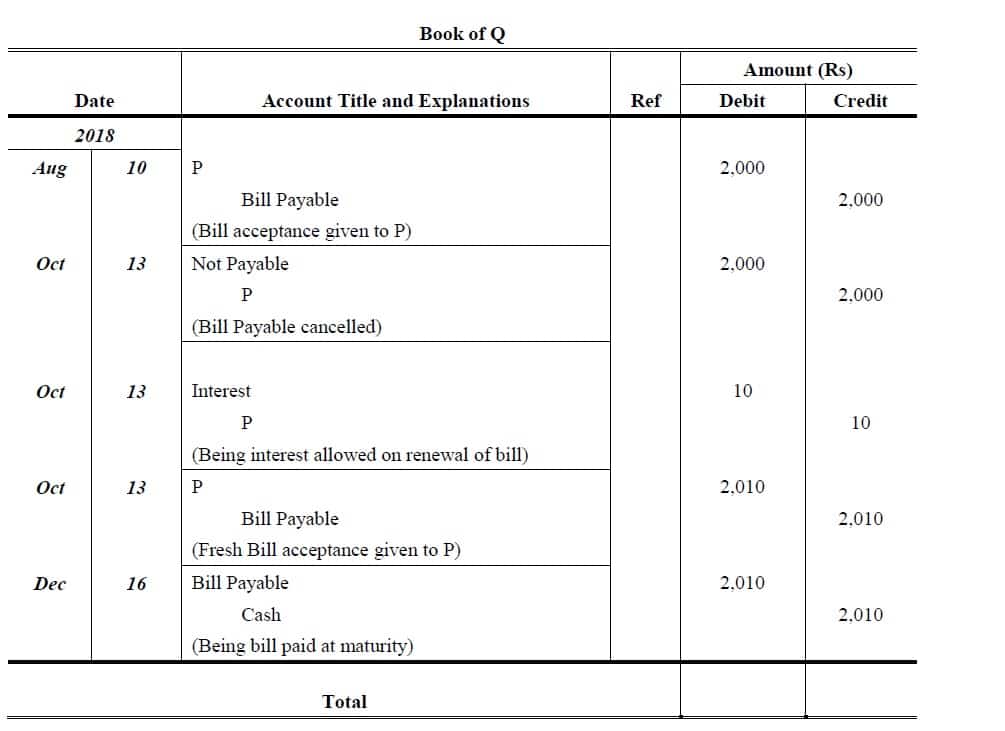

6. Renewal of a Bill of Exchange

When the acceptor of a bill finds himself unable to make payment of the bill on the due date; he may request the drawer of the bill, before it is due, to cancel the original bill and draw on him a new bill for an extended period. This is called renewing a bill of exchange. The acceptor has to pay interest for the extension of time. The new bill therefore, includes not only the amount of the original bill but also interest etc.

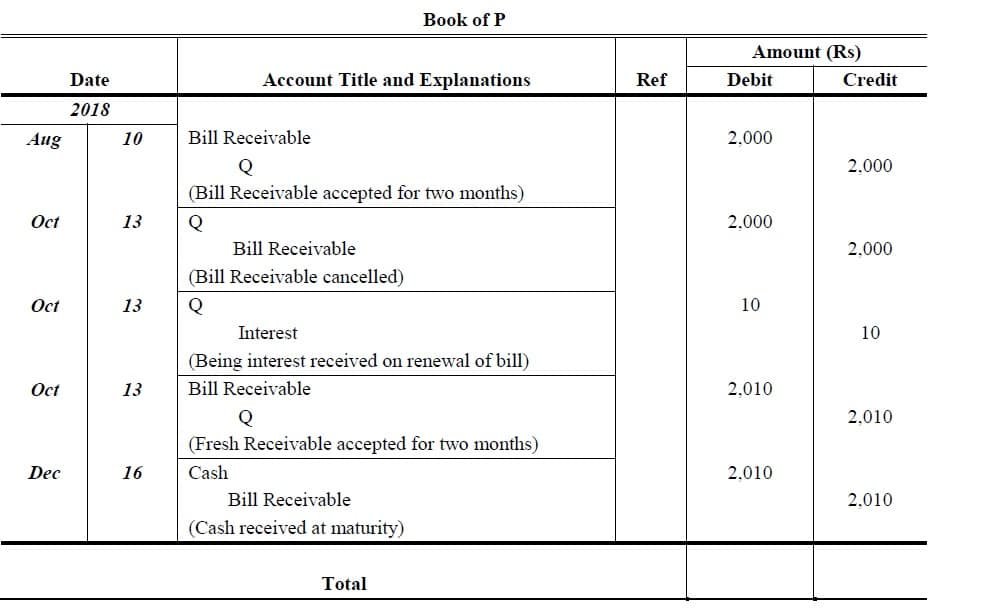

Example 6:

On August 10th, 2018 P draws a two month bill for Rs. 2,000 on Q who accepts and returns it to P. When the about to mature, Q expressed his inability to meet it and request to P to renew it for more two months. P agrees but adds Rs. 10 to the new bill for interest.

Give necessary entries in the books of P and Q from draw to last maturity.

Solution:

Related Topics

Departmental Accounts MCQs

Departmental Accounts Problems

Company Final Accounts MCQs

Company Final Accounts Problems

More Interest

Bill of Exchange Problems

References

Ramchandran, N., & Kakani, R. K. (2007). Financial Accounting for Management. (2nd, Ed.) New Delhi: Tata McGraw Hill.

Sehgal, A., & Sehgal, D. (n.d.). Advanced Accountancy (Vol. I & II). New Delhi: Taxmann Publication Pvt. Ltd.

Shukla, M. C., Grewal, T. S., & Gupta, S. C. (2008). Advanced Accountancy (Vol. I & II). New Delhi: S Chand & Co.

Weygandt, J. J., Kimmel, P. D., & Kieso, D. E. (2012). Accounting Principles (10th ed.). Hoboken: John Wiley & Sons, Inc.

Williams, M., & Bettner, H. (1999). Accounting (The basic for business decisions). (11th, Ed.) USA: Irwin McGraw- Hill.

0 Comments