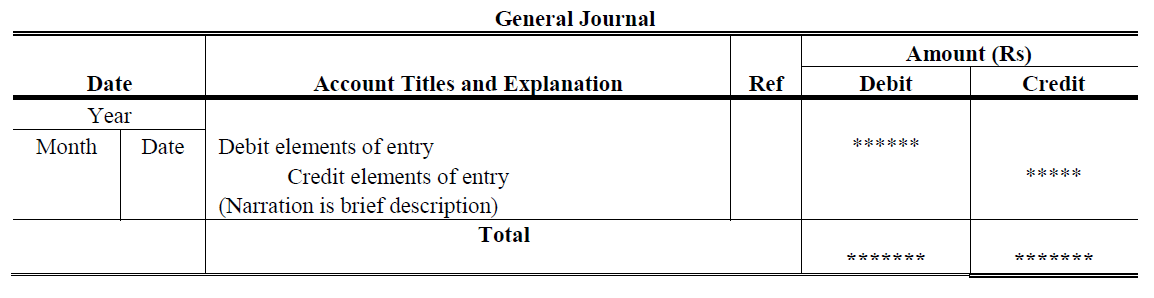

Journal Entry

Previous Lesson: Golden Rules of Accounting

Next Lesson: Accounts Receivables Journal Entry

The world Journal has been derived from French work “Jour”. Jour means day. So Journal Entry means daily up to data record of economic transaction, all transactions’ are recorder in order of their occurrences date wise (Chronological order). Every Accounting Transaction affects two or more accounts. Under Double Entry Accounting equal debit and credit entries are made for every economic activity. Journal entry is made in the book of original entry. It is first recording step. It records transactions in chronological order. Every transaction is to be recorded in journal. Every organization has to maintain one journal book at least, and general journal is general purpose book of prime entry. Entering transaction data in the journal is known as journalizing. The journal makes three significant contributions to the recording process:

- The journal discloses in one place the complete effect of a transaction

- The journal entry provides a chronological record of transactions

- The journal helps prevent or locate errors because the debit and credit amounts for each entry can be readily compared

>> Practice Journal Entry MCQs.

Video Lecture: Journal Entry in Urdu & Hindi-Workbook Practice

Parts of Journal Entry

Single record of the business transaction is called entry. We use this term to describe record transaction in Book of Accounts. There are three parts of journal entry. First write in first line just after date line is debit, second must write in below line after indented ten spaces from data line is credit and last part is narration which is brief description of transaction write within parenthesis.

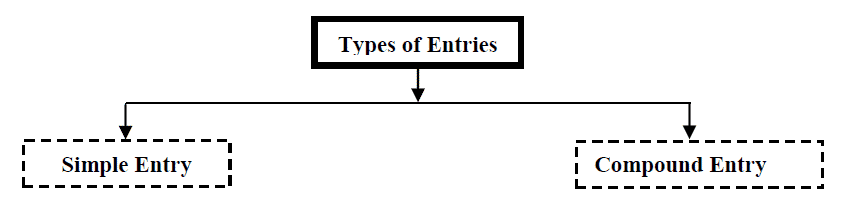

Types of Journal Entry

There are two types of journal entry. First is simple entry and second is compound entry. Simple Entry has one Debit and one Credit while, Compound Entry has more than on Debit or more than one Credit or more than one Debit and Credit.

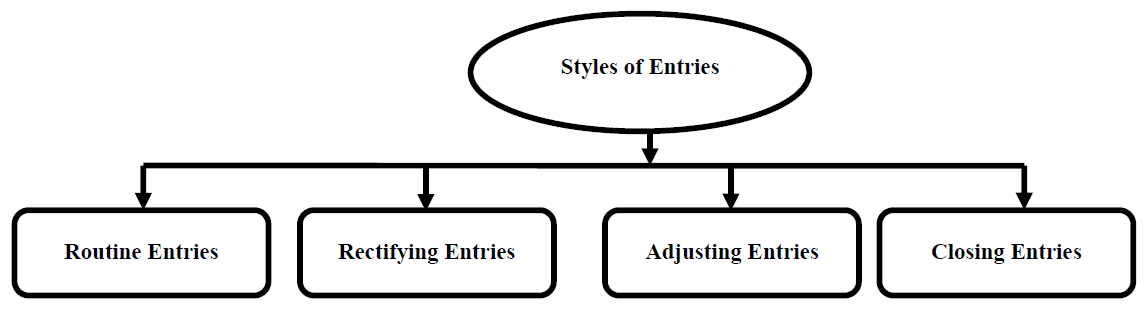

Styles of Journal Entry

There are four styles of journal entry. Following figure describes:

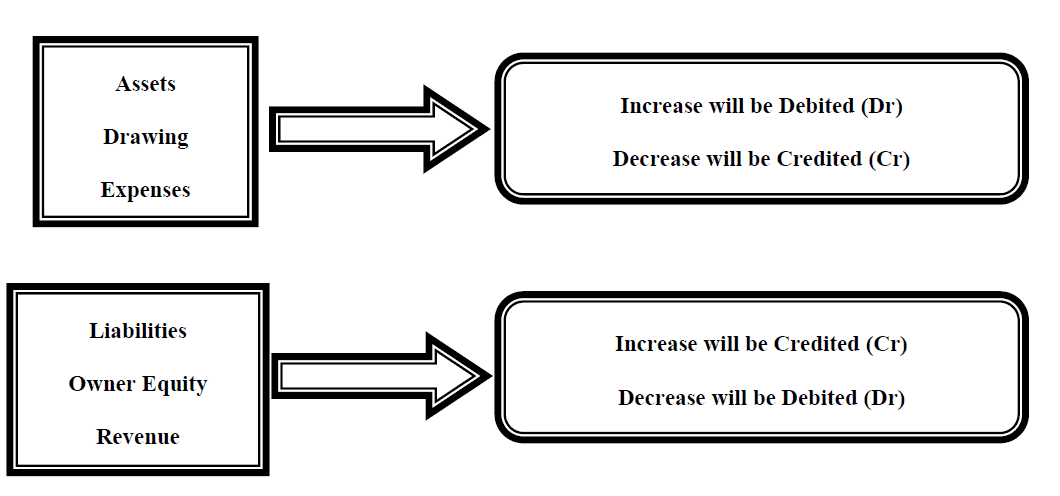

Golden Rules of Accounting

Below Golden Rules of Accounting is based on Six Pillars of Accounts. If we divide six Types of Accounts into two groups. First group contains Assets, Drawing and Expenses have ruled that increase will be Debited and decrease will be Credited. The second group contains Liabilities, Owner Equity and Revenue has ruled that decrease will be Debited and increase will be Credited. Now we would like to apply these rules one by one:

>> Practice Journal Entry Examples.

Discount

Discount is reduction in listed price. There are two types i.e. Trade Discount and Cash Discount (if not mention than also cash discount). Trade Discount is not considering for entry while entries are passed for cash discount.

Ghani, M. A. (1992). Principles of Accounting. (13th, Ed.) Lahore: Pak Imperial Book Depot.

Gupta, R. L., & Radheswamy, M. (2009). Advanced Accountancy (Vol. I & II). New Delhi: S Chand & Co.

Jain, S. .., & Narang, K. N. (2014). Advanced Accountancy. New Delhi: Kalyani Publishers.

Maheshwari, S. N., & Maheshwari, S. K. (2009). An Introduction to Accountancy. (10th, Ed.) New Delhi: Vikas Publishing House Pvt. Ltd.

Maheshwari, S. N., & Maheshwari, S. K. (2009). Financial Accounting. (5th, Ed.) New Delhi: Vikas Publishing House Pvt. Ltd.

I really like reading through an article that will make people think. Also, thanks for permitting me to comment!

My family members always say that I am killing my time here at

net, however I know I am getting experience everyday by

reading these good posts.

This site very useful and data is good, early understanding

Thank you so much and update about GST.

constantly i used to read smaller content which also clear their motive, and that is also happening with this

piece of writing which I am reading at this place.

Hi, I do believe this is an excellent blog. I stumbledupon it 😉 I may revisit yet

again since I bookmarked it. Money and freedom is the best

way to change, may you be rich and continue to help other people.

Keep functioning ,terrific job!

Sweet internet site, super pattern , real clean and utilize genial.