Direct Write Off Method

Previous Lesson: Bad Debts

Next Lesson: Allowance Method

Under direct write off method a specific account is determined to be uncollectible, the loss is charged to Bad Debts expense. Bad debts expense will show only actual losses from uncollectible. Using the direct write off method, entries to record write-offs are often made in a period following sales rather than in the period in which the sales were made. Therefore, there is no matching of expenses with the revenue.

- Use of the direct write off method can reduce the usefulness of both the Income Statement and Balance Sheet

- Unless bad debt losses are insignificant, this method is not acceptable for financial reporting purposes

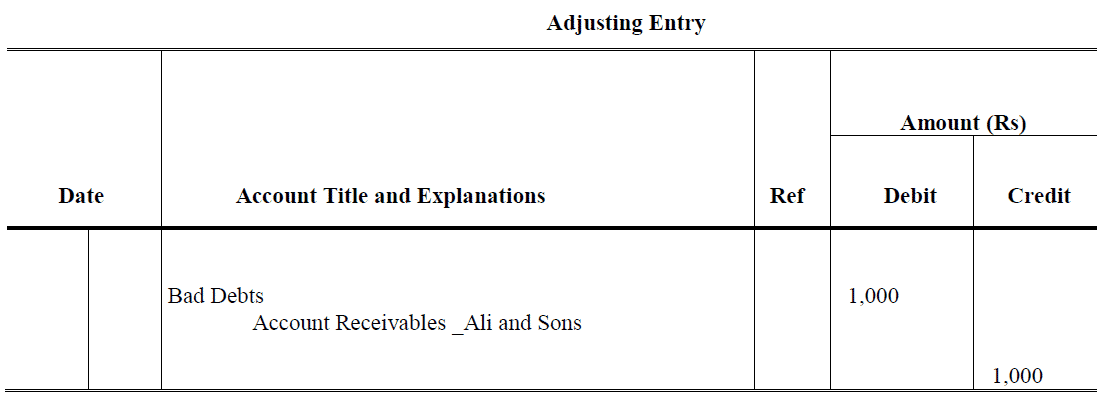

Example # 1:

Based on an analysis the bad debts expense adjustment for the year 2016 is Rs. 1,000 for Ali and Sons.

Solution:

References

Mukharji, A., & Hanif, M. (2003). Financial Accounting (Vol. 1). New Delhi: Tata McGraw-Hill Publishing Co.

Narayanswami, R. (2008). Financial Accounting: A Managerial Perspective. (3rd, Ed.) New Delhi: Prentice Hall of India.

Ramchandran, N., & Kakani, R. K. (2007). Financial Accounting for Management. (2nd, Ed.) New Delhi: Tata McGraw Hill.

0 Comments