Deferral Adjustment

Previous Lesson: Adjusting Entries

Next Lesson: Accrual Adjustment

To defer means to postpone or delay. Deferral are Costs or revenues that are recognized at a date later than the point when cash was originally exchanged. Companies make deferral adjustment to record the portion of the deferred item that was incurred as an Expenses or earned as Revenue during the current accounting period. The two types of deferral are:

- Prepaid Expenses and

- Unearned Revenues

Prepaid Expenses

Expenses paid in cash and recorded as assets until they are used or consumed are Called Prepaid Expenses. This is first type of deferral adjustment. Prepaid expenses are costs that expire with the passage of time (i. e. rent and insurance) or through use (i. e. supplies). Expenses are paid in advance are called prepaid expenses or unexpired expenses. Cost always has two parts one is expired and other on is unexpired. It is not unlikely that some expenses may have been paid in advance.

Companies record payments of expenses that will benefit more than one accounting year. Examples of common prepayments are insurance, supplies, advertising, and rent. In addition, companies make prepayments when they purchase buildings and equipment. Prepaid expenses are costs that expire either with the passage of time (e.g., rent and insurance) or through use (e.g., supplies). The expiration of these costs does not require daily entries, which would be impractical and unnecessary.

Example # 1:

On September 1, 2015 full year insurance paid of Rs. 24,000.

Solution:

We will utilize this expense for 12 months and we have 4 months expense for 2015 and remaining for 2016. Prepaid expenses has two cases on the basis of journal entry and Trial Balance presentation.

- Expense Method

- Asset Method

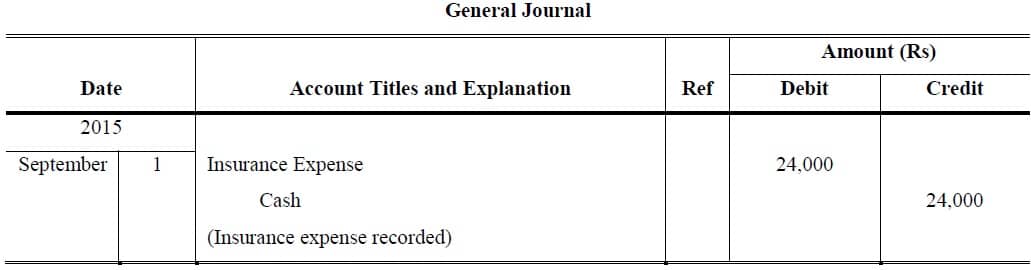

Case 1: Expense Method

Under Expense Method of deferred adjustment, following Journal Entry is pass as routine matter at September 1, 2015:

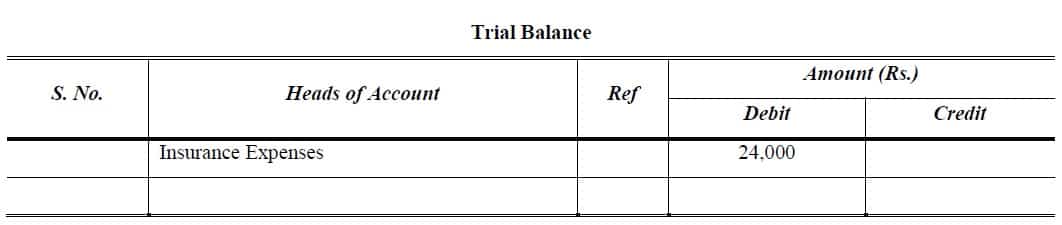

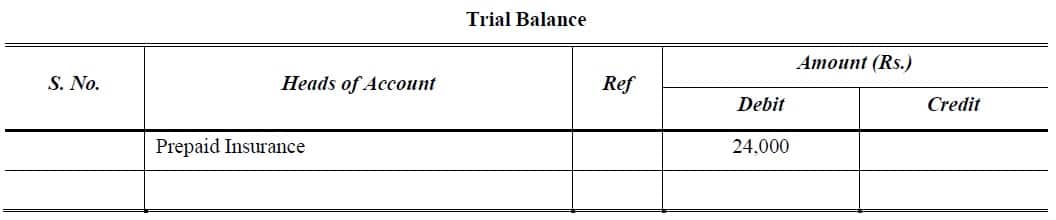

in above journal entry all complete amount of insurance is consider as expense. The effect of above regular entry in end of year trial balance (at he end of December, 2015) is presented below:

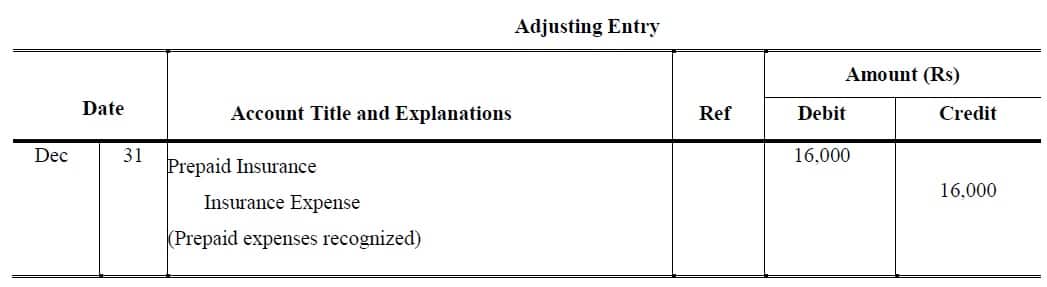

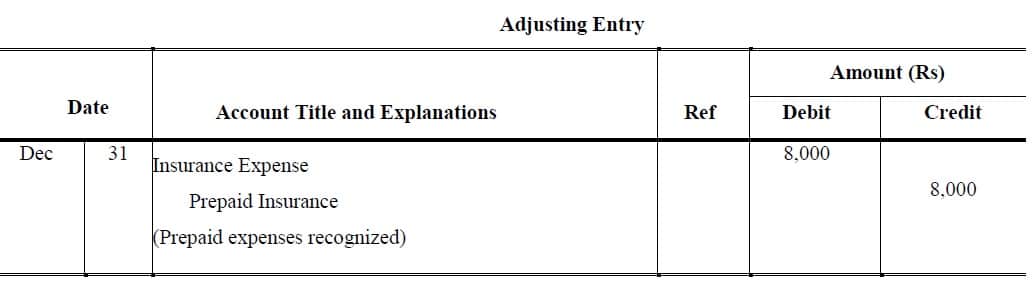

So adjusting entry at December 2015 in order to adjust the balance is presented below:

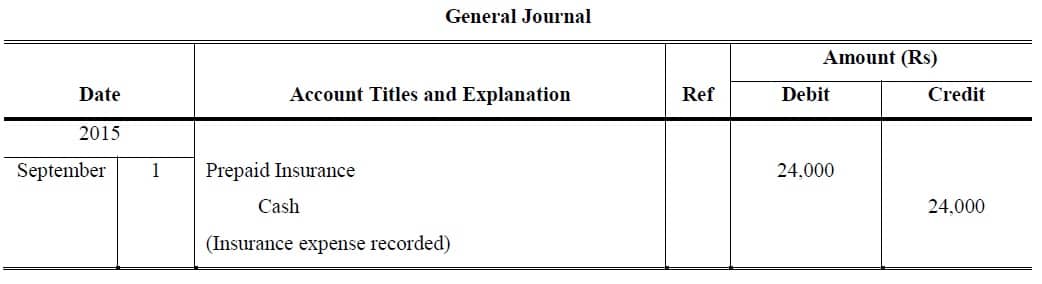

Case 2: Asset Method

Under Asset Method of deferred adjustment, all amount consider as an Assets, following journal entry is pass as routine matter at September 1, 2015:

The effect of above regular entry in end of year trial balance is presented below:

So adjusting entry at December 2015 in order to adjust the balance:

>> Adjusting Entries Problems PDF Download and Practice manually.

Unearned Revenue

Unearned Revenue is second type of deferral adjustment. Income received in advance but has not been earned in accounting period is called Unearned Revenue. There are some items of Income Statement such as interest, rent, discount etc. etc. which might have been received in advance for which the services in full has not been given so for. Companies record cash received before Revenue is earned by increasing (crediting).

Example # 2:

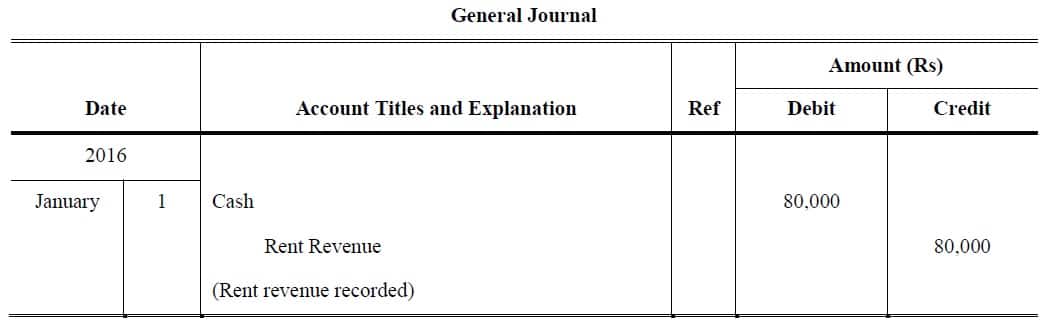

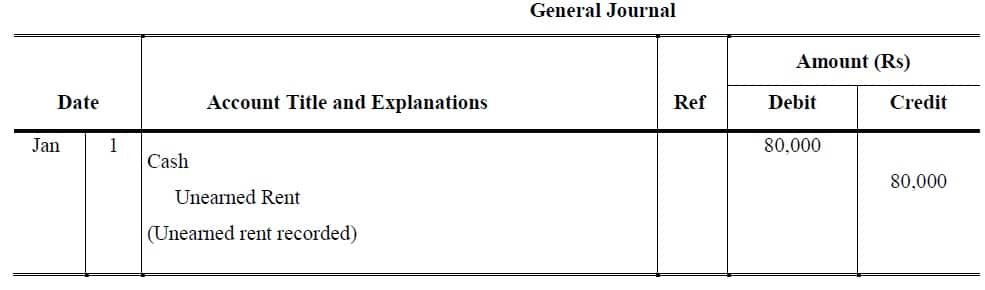

Rent received for four year in January 01, 2016 of Rs. 80,000?

Solution:

At the end of 2016 accounting period only one year rent is recognized as revenue and remaining Liabilities for next accounting year:

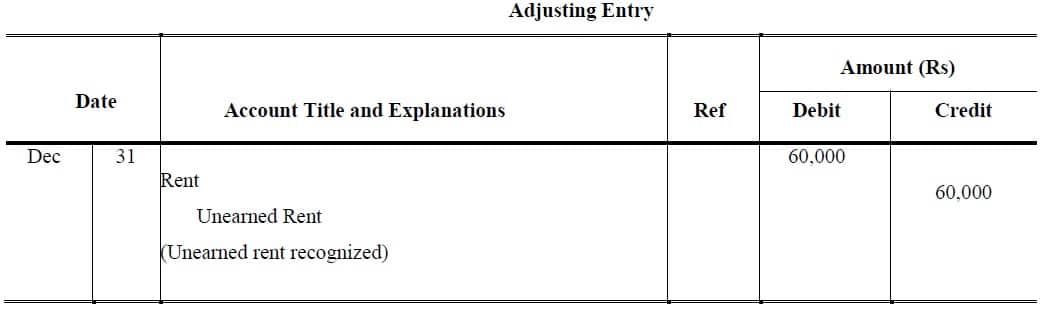

Case 1. Revenue Method

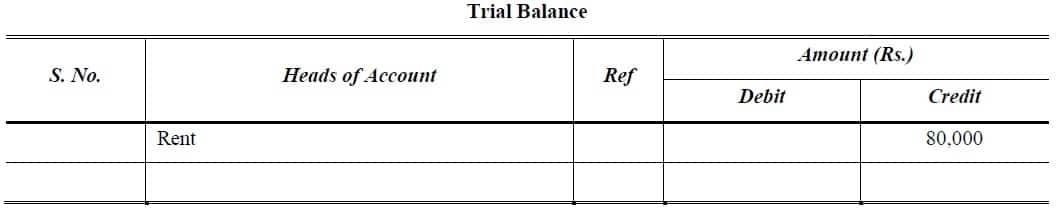

The effect of above regular entry in end of year Trial Balance is presented below:

So Adjusting Entry at December 2016 in order to adjust the balance is show below:

>>> Read and Practice Adjusting Entries Examples.

Case 2: Liability Method

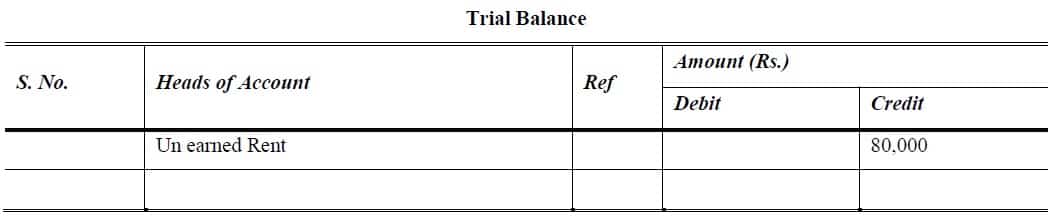

The effect of above regular entry in end of year trial balance is presented below:

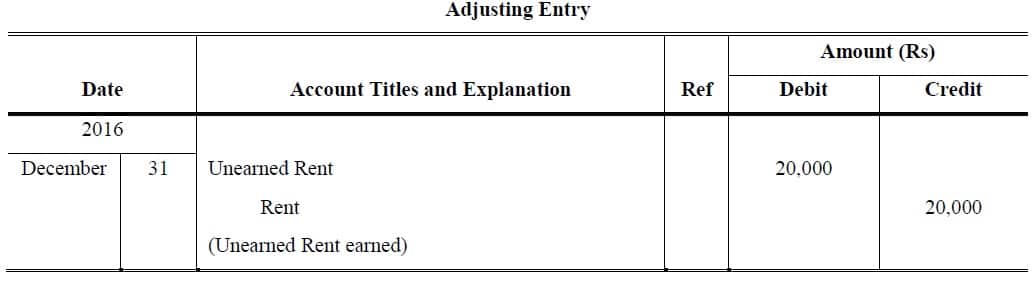

So adjusting entry at December 2016 in order to adjust the balance:

Deferred…Expenses…Assets…Prepayments

Deferred…Revenue…Liability…Unearned

>>> Practice Adjustment Entries Quiz 1.

References

Mukharji, A., & Hanif, M. (2003). Financial Accounting (Vol. 1). New Delhi: Tata McGraw-Hill Publishing Co.

Narayanswami, R. (2008). Financial Accounting: A Managerial Perspective. (3rd, Ed.) New Delhi: Prentice Hall of India.

Ramchandran, N., & Kakani, R. K. (2007). Financial Accounting for Management. (2nd, Ed.) New Delhi: Tata McGraw Hill.

I can see that you are a specialist at your area! I am starting a website soon, and your tips will be very valuable for me.. Thanks for all your support and wishing you all the success in your business.