Rectification of Errors

Previous Lesson: Trial Balance

Next Lesson: Correcting Entries

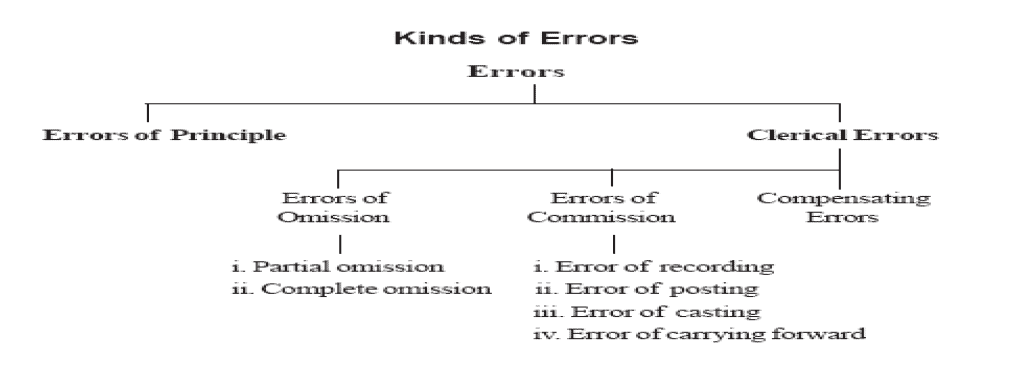

Errors are unintentional misstatement or omission or mistake committed in Books of Accounts. The mistakes may be one relating to routine or one relating to principle. Following are most common error encountered in accounting records:

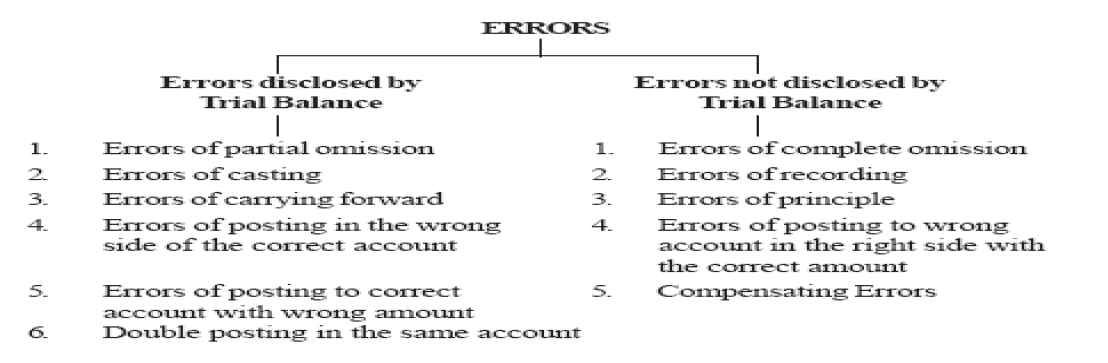

Errors in Trial Balance

Errors in Trial Balance are classified as errors disclosed by trial balance and errors not disclosed by trial balance.

Locating Errors

Following nine steps will follow in order to locate errors:

Step 1: Make sure balances in trial balance in correct sides.

Step 2: Check whether the Debit and Credit sides added correctly by opposite direction.

Step 3: Divide the difference by 9. If divisible by 9, so transposition error or slide error. If digits are place wrongly i.e. 5,760………. 5,670

Or

6,250 ………………….. 62.50 (decimal point transposition error).

Step 4: Divide the difference by 2, and check the identical amount in the bigger columns of trial balance.

Step 5: Check ledger account if shows an account equal to difference.

Step 6: Cross checking the amount in trial balance and ledger accounts.

Step 7: Re-compute the balance of each ledger.

Step 8: Check posting from journal to ledger

Step 9: Check journal entries in detail.

>> For Practice See Rectification of Errors MCQs

Video Lecture: Rectification of Errors in Urdu & Hindi-Workbook Practice

Rectification of Errors Examples

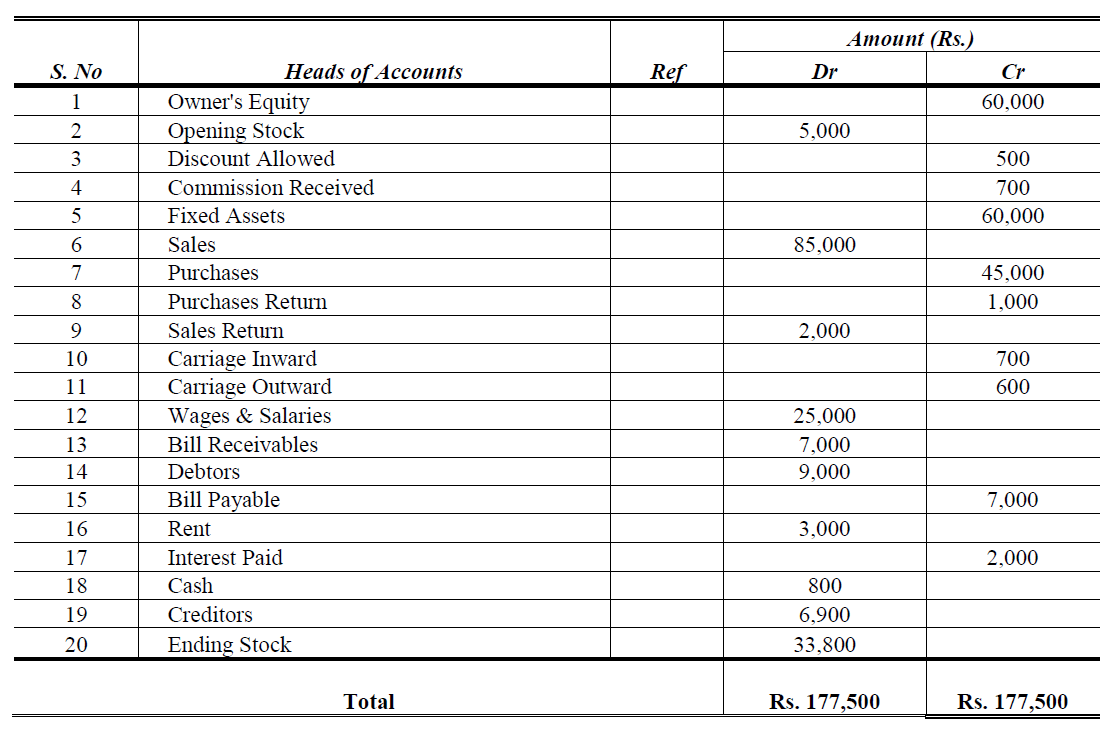

Example 1:

The clerk of ABC business wrongly prepared the following trial balance. You are required to draw up a trial balance correctly?

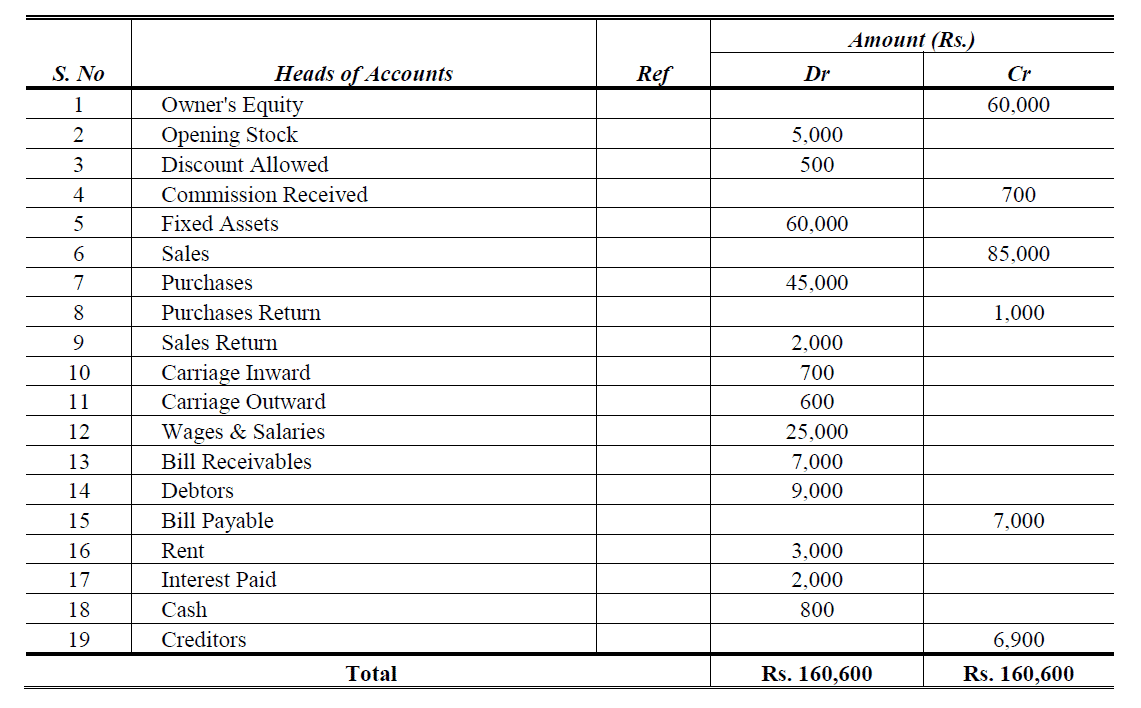

Solution:

>> Practice on paper with Rectification of Errors Problems and Solutions.

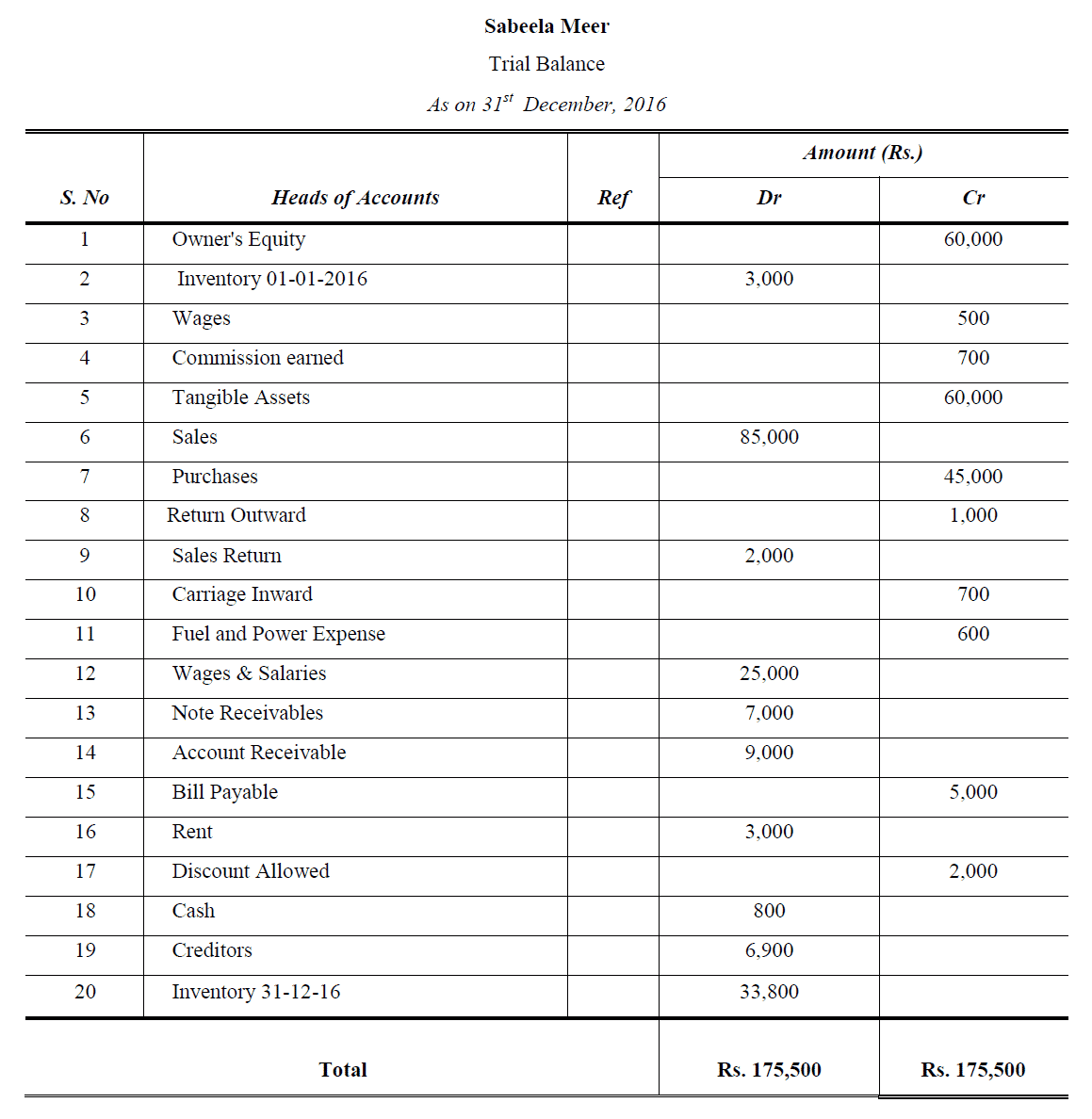

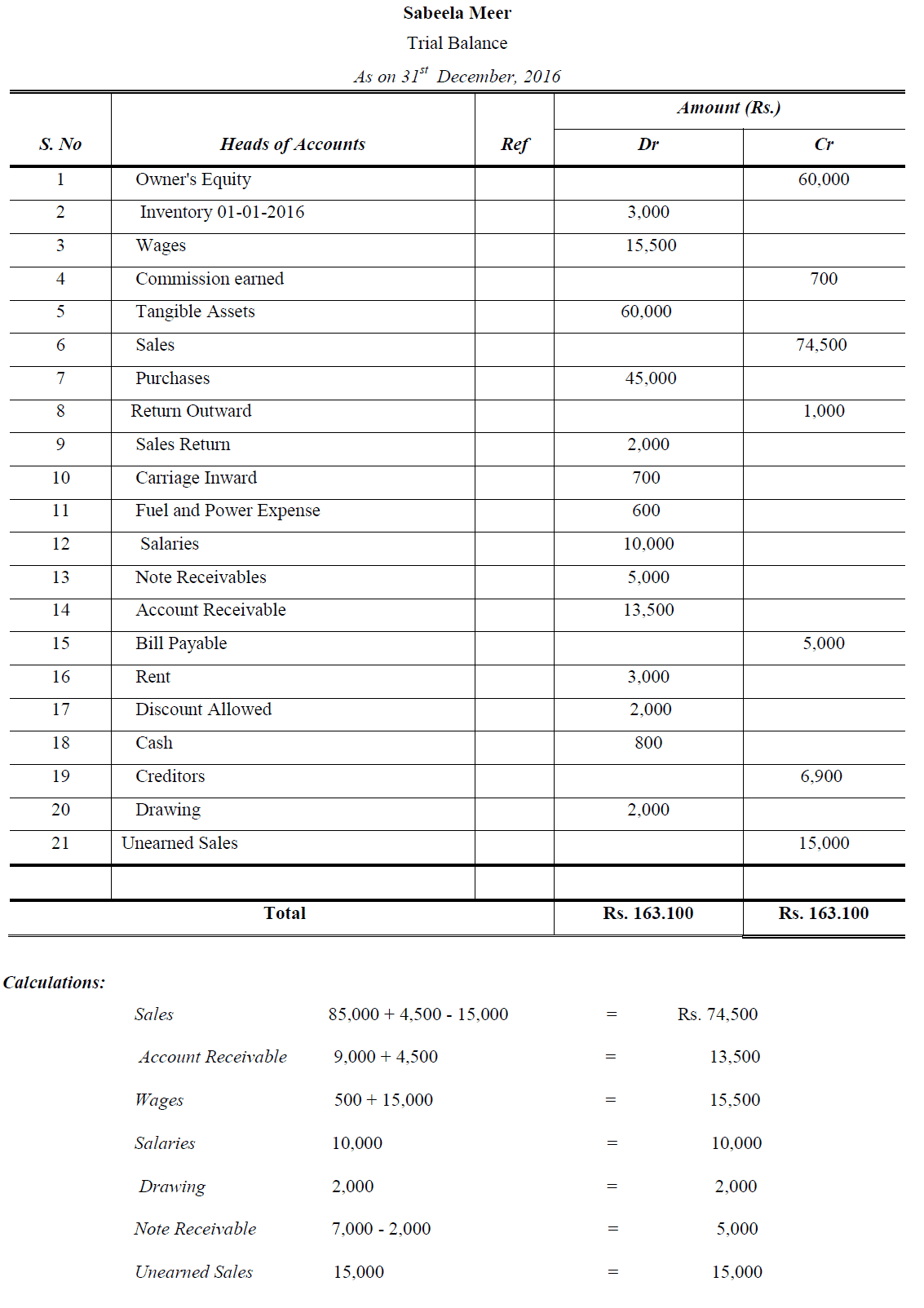

Example 2:

The Make corrected trial balance after anticipating hidden errors?

Errors:

Credit sales of worth Rs. 4,500 was omitted to record in the book of original entry.

Wages and Salaries account should be separate to Rs. 15,000 and 10,000 respectively.

Drawing of worth Rs. 2,000 wrongly charged to Note Receivable Account.

Unearned Sales of Rs. 15,000 was incorrectly credited to Sales Account.

Following accounts are used for correction and adjusting the transactions.

Sales; Account Receivable; Wages; Salaries; Drawing; Note Receivable; Unearned Sales

Solution:

References

Mukharji, A., & Hanif, M. (2003). Financial Accounting (Vol. 1). New Delhi: Tata McGraw-Hill Publishing Co.

Narayanswami, R. (2008). Financial Accounting: A Managerial Perspective. (3rd, Ed.) New Delhi: Prentice Hall of India.

Ramchandran, N., & Kakani, R. K. (2007). Financial Accounting for Management. (2nd, Ed.) New Delhi: Tata McGraw Hill.

0 Comments