Chart of Accounts

Previous Lesson: Accounting Variation Proforma

Next Lesson: Contra Account

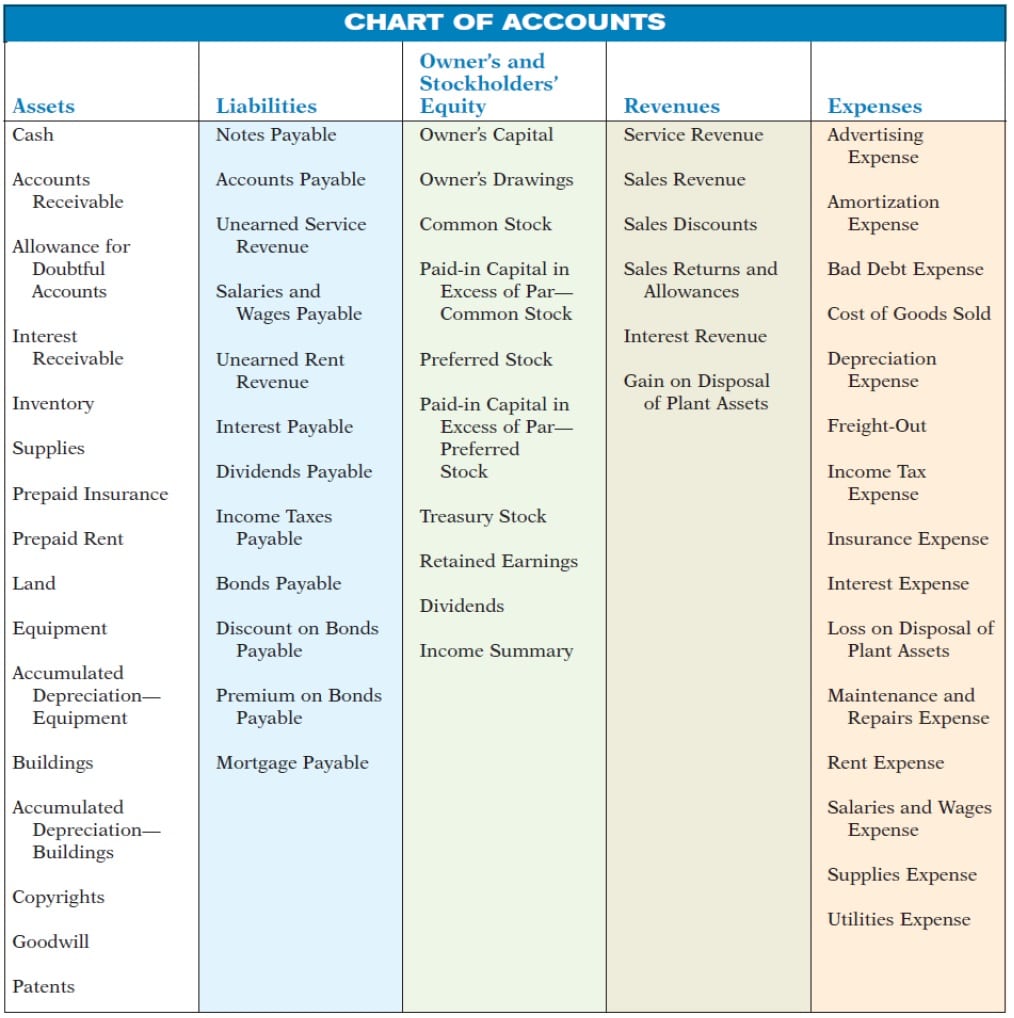

Chart of Accounts is a list of General Ledger account names and numbers arranged in the order in which they appear in the Financial Statement. Account is formal record that represents certain resources and claims to such resources, transactions or other events that result in changes to those resources and claims. This chart of accounts serves as a useful source for locating a given account within the ledger. The numbering system for the chart of accounts must leave room for new accounts. A range of numbers is assigned to each financial statement category.

Listing all the accounts of an organization in the general ledger is known as charts of accounts. It is the created list of all the accounts that define each class of items for which the money is received or spent within an organization. We can also say that COA is the official accounting term that displays both the income statement accounts and the balance sheet accounts. Chart of accounts break down the accounts into the subcategories. In order to identify the accounts type a multi-digit number is assigned to each chart in the list. Chart of account includes the brief description of the accounts, its name, and the identification codes of all the accounts. The length of account numbers is usually five or more digits and each digit represents the type of account, the division of company and the department. First the balance sheet accounts are listed and then the income statement accounts.

A company’s charts of accounts are as complex and large as the company itself is. A large corporation needs thousands of accounts if it has several departments because every department has its own charts of accounts whereas in small businesses such as the retail business there are only few accounts. The accounts are mostly numerical but in some cases they can also be alphanumerical and alphabetical.

Types of Accounts

The following types of accounts are included in the charts of accounts:

Assets

Assets are anything that are owned by a person or a company or that is controlled by an entity. Assets accounts include:

Machinery, Furniture, Leasehold Premises, Building, Equipment, Plant, Account Receivables, Note Receivables, Land, Car, Marketable Securities, Cash, Goodwill, Leasehold building, Bank, Computer, Fixture and Fittings, Copy Rights, Leasehold land, Inventories, Loan to employees, Prepaid items etc. etc.

Drawing

Drawings Account is any withdrawal made by Owner in the form of physical assets like furniture, inventory etc. or in the form of Financial asset like cash etc.

Expense

Expenses are outflows, for instance, Wages, Salaries, Rent, Freight, Carriage, Repairs, Maintenance, Discount, Rebate, Transportation, Commission, Miscellaneous Expense, and Entertainment Expense (which have debit balance or paid).

Liability

The legal obligations of the company are known as Liabilities. These include:

Note Payable, Account Payable, Bank Loan, Debenture, Bonds, Mortgage Loan and any outstanding or payables and unearned.

Owner Equity or Shareholders’ Equity

Any assets invested by owner may be in form of monetary or physical assets. The residual equity of the owner is known as shareholders equity or Owner’s Equity. It includes:

- Retained earnings

- Preferred stock

- Common sock

Revenue

Sales, fees etc. all accounts have credit balance like commission (Cr) or received like discount received. The earnings of the company are listed in the Revenue Accounts. Revenue accounts include:

- Sales

- Income

Contra Accounts

The accounts that offset all the other accounts of the balance sheets or that have the negative balance is known as the contra accounts. These accounts include:

- Sales return

- Purchase return

- Allowances in bad debts

- Accumulated depreciation

The number and type of accounts differ for each company. The number of accounts depends on the amount of detail management desires. For example, the management of one company may want a single account for all types of utility expense. Another may keep separate expense accounts for each type of utility, such as gas, electricity, and water. Most companies have a chart of accounts. This chart lists the accounts and the account numbers that identify their location in the ledger. The numbering system that identifies the accounts usually starts with the balance sheet accounts and follows with the income statement accounts.

>> Read Types of Accounts.

References

Maheshwari, S. N., & Maheshwari, S. K. (2009). Financial Accounting. (5th, Ed.) New Delhi: Vikas Publishing House Pvt. Ltd.

Maheshwari, S. N., & Maheshwari, V. L. (2009). Advanced Accountancy (Vol. I & II). New Delhi: Vikas Publishing House Pvt. Ltd.

Mukharji, A., & Hanif, M. (2003). Financial Accounting (Vol. 1). New Delhi: Tata McGraw-Hill Publishing Co.

Narayanswami, R. (2008). Financial Accounting: A Managerial Perspective. (3rd, Ed.) New Delhi: Prentice Hall of India.

Porwal, L. S. (2001). Accounting Theory. New Delhi: Tata Mcgraw Hill Publishing Co. Ltd.

What is the ledger of this jurnal entry

You are doing a good job. still u cant call it great bcuz uve not really posted the reasons for ur choosings regarding the entries.