Cash Flow Statement

Previous Lesson: Fund Flow Statement

Next Lesson: Closing Entries

Four major financial statements are required for external reports, which are an income statement (statement of comprehensive income), a statement of owner’s equity (statement of changes in equity), a Balance Sheet (statement of financial position) and a cash flow statement (statement of cash flows).

The purpose of the cash flow statement is to highlight the major activities that directly and indirectly impact cash flows and hence affect the overall cash balance. In preparing a statement of cash flows, the term cash is broadly defined to include both cash and cash equivalents. It is a summary of a firm’s cash receipts and cash payments during a period of time. Statements of cash flow classified into three sections:

- Operating Activities,

- Investing Activities and

- Financing Activities

>>> See also Fund Flow Statement

The cash flow statement may be presented using either a “direct” method or an “indirect” method. The only difference between the direct and indirect methods of presentation concerns the reporting of operating activities; the investing and financing activity sections would be identical under each method. The cash flow statement is usually divided into three sections: Operating, Investing and Financing activities.

1. Operating Activities (Indirect Method)

First of all it is important to note that you required current year Income Statement and two years balance sheet for preparing cash flow statement. Following steps are used to calculate cash flow from operating activities under the indirect method:

- Start with net profit.

- Add non-cash expenses, such as depreciation, amortization and depletion that are already included in net income.

- Less non-cash gains, such as gain on sale of assets.

- Add or Less changes in working capital excluding short term borrowing (not payable and like nature) and cash equivalents (cash in hand, cash at bank and marketable securities). Working capital is current assets and current liabilities.

- Inflow of cash is any decrease in non-cash current asset or any increase in current liability. Outflow of cash is any increase in non-cash current asset or any decrease in current liability:

| Inflow of Cash | Outflow of Cash |

| Any decrease in non-cash current asset | Any increase in non-cash current asset |

| Any increase of current liability | Any decrease in current liability |

In another way we can show above concepts in below mention table:

| Non-cash Current Assets | Current Liability (Excluding N/P) | |

| Inflow | Decrease | Increase |

| Outflow | Increase | Decrease |

Example # 1:

UMAR FAROOQ Company’s current asset and liability balances for the past two years are as follows. Net income for the year was Rs. 120,000 and depreciation expense was Rs. 15,000.

| December 2016 | December 2017 | |

| Accounts receivable | Rs. 80,000 | Rs. 65,000 |

| Inventory | Rs. 130,000 | Rs. 140,000 |

| Accounts payable | Rs. 45,000 | Rs. 40,000 |

| Accrued liabilities | Rs. 12,000 | Rs. 15,000 |

Required: You are require to prepare operating activities section of cash flow statement?

Solution:

UMAR FAROOQ

Cash Flow Statement

For the year ended December, 2017

| Operating Activities: | |

| Net income | Rs. 120,000 |

| Depreciation | 15,000 |

| Decrease in accounts receivable | 15,000 |

| Increase in inventory | (10,000) |

| Decrease in accounts payable | (5,000) |

| Increase in accrued liabilities | 3,000 |

| Net cash flow from operating activities | Rs. 138,000 |

Example # 2:

Zainab Iftikhar Corporation’s current asset and liability balances for the past two years are as follows. Net income for the year was Rs. 150,000, depreciation expense was Rs. 22,000, and gain on sale of land was Rs. 28,000.

| June 2016 | June 2017 | |

| Accounts receivable | Rs. 80,000 | Rs. 92,000 |

| Inventory | Rs. 120,000 | Rs. 110,000 |

| Accounts payable | Rs. 35,000 | Rs. 30,000 |

| Accrued liabilities | Rs. 12,000 | Rs. 8,000 |

Required: Using the indirect method, prepare the cash flows provided by operating activities section of the statement of cash flows.

Solution:

Zainab Iftikhar

Cash Flow Statement

For the year ended June, 2017

| Operating Activities: | |

| Net income | Rs. 150,000 |

| Depreciation | 22,000 |

| Gain on sale of land | (28,000) |

| Increase in accounts receivable | (12,000) |

| Decrease in inventory | 10,000 |

| Decrease in accounts payable | (5,000) |

| Increase in accrued liabilities | (4,000) |

| Net cash flow from operating activities | Rs. 133,000 |

2. Investing Activities

Investing activities generally involve in the cash flows of non-current assets which are long term investment and fixed assets. Important accounts for investing activities show below:

| Cash Flow from Investing Activities | |

| Sales of machinery | ****** |

| Payment for long term investment | (******) |

| Cash paid to buy plant and equipment | (******) |

| Cash received from selling a building | ****** |

| Net Cash Flow from Investing Activities |

3. Financing Activities

Financing activities involve cash flow of short term borrowing (not payable and like nature), long term liabilities shareholder’s equity and dividend.

Example # 3:

Usama Ali Khan Company experienced the following at end of year, December 2017:

- Issued preferred stock for Rs. 250,000

- Repurchased Rs. 140,000 of its own common stock

- Borrowed Rs. 200,000 from a bank issuing a 5 year note

- Retired bonds by paying Rs. 55,000

- Declared dividends of Rs. 135,000 payable on March 1, 2018

Required: Prepare the financing section of the statement of cash flows.

Solution:

Usama Ali Khan

Cash Flow Statement

For the year ended December, 2017

| Financing Activities: | |

| Issued preferred stock | Rs. 250,000 |

| Repurchased of its own common stock | (140,000) |

| Borrowed from a bank issuing a 5–year note | 200,000 |

| Retired bonds | (55,000) |

| Net Cash Flow from Financing Activities | Rs. 255,000 |

Checking Point:

We can check prepared cash flow statement with the help of cash and cash equals. Last year Cash Equals + Changes in Cash Equals = Current year Cash Equals.

| Increase in Cash and Cash Equivalents | ****** |

| Cash and Cash Equivalents in Last year | **** |

| Cash and Cash Equivalents in Current year | **** |

Steps for cash flow statement

Preparing the statement of cash flow involves five steps, having two year balance sheet and current year income statement:

- Determine the net cash flow from operating activities by direct or indirect method

- Determine net cash flows from investing activities

- Determine net cash flows from financing activities

- Determine the change in cash equals

- Last year Cash Equals + Changes in Cash Equals = Current year Cash Equals

Example # 4:

Classify each of the following items of cash flows as a Not Cash Flow, Operating, Investing and Financing Activities:

| Description | Not Cash flow | Operating | Investing | Financing |

| Repayment of bank loan | X | |||

| Purchase of new machine | X | |||

| Payment of monthly payroll | X | |||

| Issuance of bonds | X | |||

| Purchase of inventory on account | X | |||

| Pay weekly salary | X | |||

| Pay dividends | X | |||

| Receive interest on bank account | X | |||

| Exchange old delivery truck for new one and take note for balance |

X |

|||

| Sell land | X | |||

| Repurchase corporate stock | X | |||

| Sell merchandise on account | X | |||

| Collect cash from customers | X | |||

| Pay for inventory purchased | X | |||

| Payment of rent | X |

Example # 5:

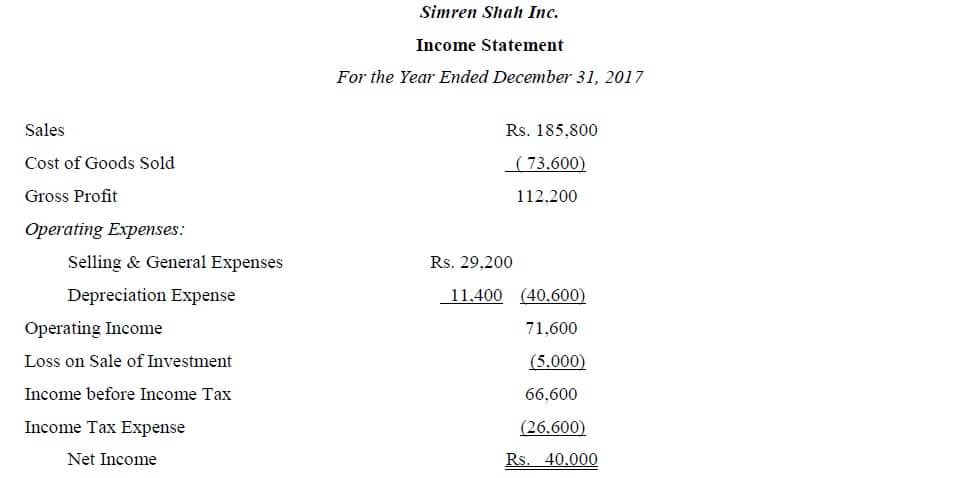

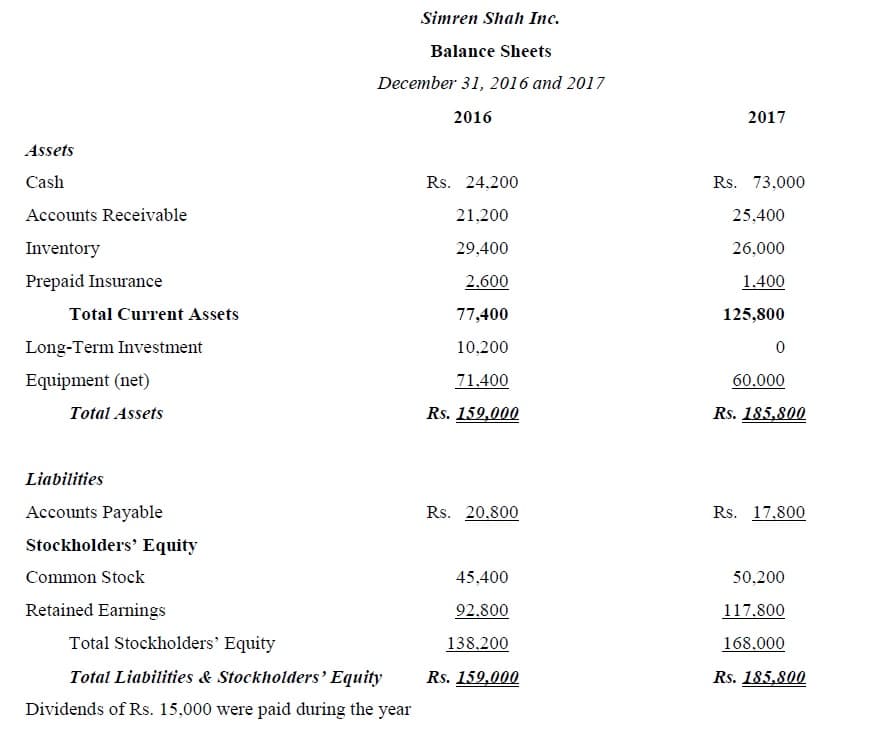

Data related to Simren Shah Inc. are presented below. Prepare a statement of cash flows, for the year ended December 31, 2017:

Solution:

Simren Shah Inc.

Cash Flow Statement

For the Year Ended December 31, 2017

| Operating Activities: | |

| Net income | 40,000 |

| Depreciation | 11,400 |

| Loss on sale of investment | 5,000 |

| Increase in accounts receivable | (4,200) |

| Decrease in inventory | 3,400 |

| Decrease in prepaid insurance | 1,200 |

| Decrease in accounts payable | (3,000) |

| Net cash flow from operating activities | 53,800 |

| Investing Activities: | |

| Sale of long term investment (10,200 – 5,000) | 5,200 |

| Net cash flow from operating activities | 5,200 |

| Financing Activities: | |

| Sale of common stock | 4,800 |

| Dividend paid | (15,000) |

| Net cash flow from financing activities | (10,200) |

| Net increase in cash | 48,800 |

| Cash at Last year | 24,200 |

| Cash at Current year | 73,000 |

Example # 6:

The following information was gathered from Waji-Ul-Hassan Corporation’s financial records at the end of December 31st, 2017:

| Net income | Rs. 65,000 |

| Depreciation expense | 12,000 |

| Beginning cash balance | 22,000 |

| Decrease in accounts receivable | 12,000 |

| Increase in inventory | 8,000 |

| Decrease in accounts payable | 6,000 |

| Decrease in accrued liabilities | 2,000 |

| Proceeds from bank loan | 25,000 |

| Payment of dividends to stockholders | 16,000 |

| Purchase of land

Cash balance at the end |

35,000

69,000 |

Required: Using the indirect method, prepare a statement of cash flows

Solution:

Waji-Ul-Hassan Corporation

Cash Flow Statement

For the Year Ended December 31, 2017

| Operating Activities: | |

| Net income | 65,000 |

| Depreciation expense | 12,000 |

| Decrease in accounts receivable | 12,000 |

| Increase in inventory | (8,000) |

| Decrease in accounts payable | (6,000) |

| Decrease in accrued liabilities | (2,000) |

| Net cash flow from operating activities | 73,000 |

| Investing Activities: | |

| Purchase of land | (35,000) |

| Net cash flow from operating activities | (35,000) |

| Financing Activities: | |

| Proceeds from bank loan | 25,000 |

| Payment of dividends to stockholders | (16,000) |

| Net cash flow from financing activities | 9,000 |

| Net increase in cash | 47,000 |

| Cash at Last year | 22,000 |

| Cash at Current year | 69,000 |

References

Mukharji, A., & Hanif, M. (2003). Financial Accounting (Vol. 1). New Delhi: Tata McGraw-Hill Publishing Co.

Narayanswami, R. (2008). Financial Accounting: A Managerial Perspective. (3rd, Ed.) New Delhi: Prentice Hall of India.

Ramchandran, N., & Kakani, R. K. (2007). Financial Accounting for Management. (2nd, Ed.) New Delhi: Tata McGraw Hill.

Thank you, wonderful job! This was the information I had to have.