Capital Budgeting

Previous Lesson: Risk and Return

Next Lesson: Payback Period

Capital Budgeting is the process of identifying, analyzing and selecting investment project whose returns (Cash Flows) are expected to extend beyond one year.

Capital Budgeting Techniques

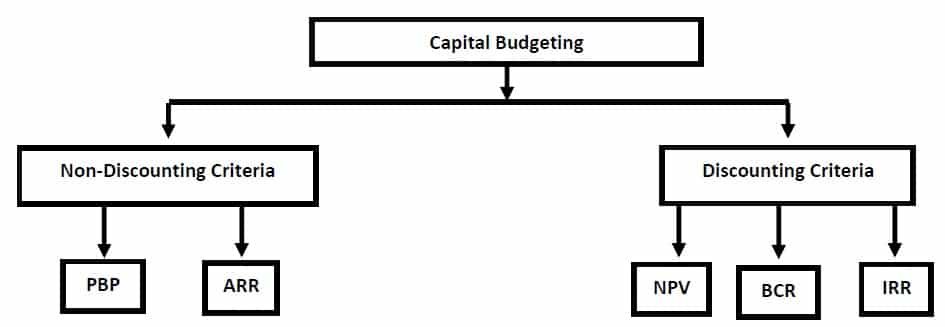

There are different methods of evaluating capital investment projects. Broadly, there are two alternative methods of project evaluation and selection used in Capital Budgeting:

Non-Discounting Criteria

Non-discounting techniques take into account magnitude and not timing of the expected cash flow ignoring time value of money. Following are different non-discount techniques:

1. Payback Period

2. Accounting Rate of Return

Discounting Criteria

Discounting cash flow method provide more objective basis for evaluating and selecting projects. This method take into account both magnitude and timing of the expected cash flow in each period of project’s life. Following are some important techniques used under Discounting Criteria:

1. Net Present Value (NPV)

2. Profitability Index (PI) or Benefit Cost Ratio (BCR)

3. Internal Rate of Return (IRR)

>> Practice Capital Budgeting Quiz 1.

Related Topics

Capital Budgeting Problems

Further Readings

References

Financial Management: Theory and Practice, Dr Eugene F Brigham & C Micheal Ehrhardt

Fundamentals of Financial Management: Concise Edition, Brigham Houston

The Economist Guide to Financial Management, John Tennet

Financial Management: Core Concepts, Raymond M Brooks

basic ideas good