Bookkeeping

Previous Lesson: Normal Balance

Next Lesson: Accrual Accounting

Define Bookkeeping

Bookkeeping can be described as, the recording of monetary transactions, appropriately classified, in the financial records of an entity, either by manual means or otherwise. Bookkeeping involves maintaining a detailed ‘history’ of transactions as they occur. Every sale, purchase or other transaction will be classified according to its type and, depending on the information needs of the organization, will be recorded in a logical manner in the books of accounts.

These books will contain a record, or account, of each item showing the transactions that have occurred, thus enabling management to track the individual movements on each record, that is, the increases and decreases. Periodically a list of the results of the transactions is produced. This is done by listing each account and its final position or balance. The list is known as a trial balance and is an important step prior to the next stage of providing financial statements.

>> See Accounting Definition.

Difference between accounting and bookkeeping

Bookkeeping should not be confused with accounting or accountancy. Persons with little knowledge of accounting may fail to understand the difference between these terms and often used to mean the same thing. Therefore, it is useful to make a distinction. Bookkeeping is a small part of the field of accounting and the simplest part, just like arithmetic is a small part of the broad discipline of mathematics. Its work is clerical nature and can be performed by office workers, machine and computers. The functions of Bookkeeping is to properly record the financial transactions in the books of account. It is recording or first phase of an accounting system.

Accounting and bookkeeping are two responsibilities, which are critical for each business organization. In the most straightforward of terms, bookkeeping is responsible for recording economic transactions, classifying term and produce initial summary of accounts. On the other hand, accounting is reasonable for analyzing and interpreting of accounting data in order to take business decisions.

>>> See Principles of Accounting Course.

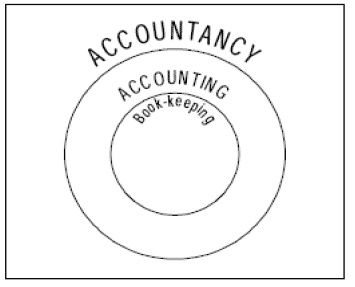

Difference between Bookkeeping, Accounting and Accountancy

Bookkeeping is basic of recording of accounts in a systematic manner. The process of accounting begins where the bookkeeping process ends. Accounting is broad subject and final phase. The function of accounting is to classify the recorded transactions, summarize them, interpret them, and collect and communicate necessary information to the management and other interested parties. Accounting includes not only maintenance of accounting records, but also the preparation and interpretation of financial Statements.

The two words accounting and accountancy are often used to mean the same thing. But it is not correct. Accountancy is the main subject while, accounting is one of its branches. The word “accountancy” is far extensive; i.e. the scope of accountancy is far a wide and extensive compared to accounting. It covers the entire body of theory and practice, e.g. bookkeeping, accounting, costing, auditing, taxation etc.

>> See for more information Accounting Basics.

Why Book-keeping is Necessity?

The main reasons for keeping record are as under:

- It is impossible for a businessman to remember all his dealings without keeping proper record for them, because everybody has been gifted by nature with a limited memory. Therefore, proper record must be maintained to obtain the required information for efficient and smooth running of the business so that misunderstanding, wastes, fraud and errors may be checked.

- From the income tax point of view, a proper record is indispensable; otherwise the traders will be at the mercy of the income tax authorities for the purpose of taxation.

- Book-keeping is a written history of a business in terms of money or finances. Just as the study of history tells the past facts and at the same time gives the guidance for the right steps to the taken in future. In the same way the study of book-keeping record reveals the past financial position of a business and at the same time guides the business man the necessary steps to be taken for further improvement in it in future.

- Bookkeeping record provides an easy way of comparing the financial position of a business for different periods.

- Proper book-keeping record gives correct information about cash resources both in hand and at bank.

- If it becomes necessary at any time to dispose of an existing business, the selling price of the business can be easily and correctly ascertained provided a proper record is maintained.

- If a trader fails in his business, he may have to submit his records before the insolvency court for final disposal of his business but in the absence of proper record he cannot receive any mercy from the court.

Important books of accounts for Bookkeeping

The ledger is the only book of account, so called because all the transactions after being first recorded in books of original or prime entry or subsidiary books are afterward grouped or summarized in accounts in the ledger. The following are the books of original entry used in book-keeping.

- Journal

- Cashbook

- Purchase book

- Purchase return and allowance book

- Sales book

- Sales return and allowance book

- Bill receivable book

- Bill payable book

References

Mukharji, A., & Hanif, M. (2003). Financial Accounting (Vol. 1). New Delhi: Tata McGraw-Hill Publishing Co.

Narayanswami, R. (2008). Financial Accounting: A Managerial Perspective. (3rd, Ed.) New Delhi: Prentice Hall of India.

Ramchandran, N., & Kakani, R. K. (2007). Financial Accounting for Management. (2nd, Ed.) New Delhi: Tata McGraw Hill.

This is a fantastic post!

Thank you for explaining the differences between bookkeeping, accounting, and accountancy. Also, the significance of bookkeeping is well defined.