Adjusted Trial Balance

Previous Lesson: Allowance Method

Next Lesson: Financial Statement

After a company has journalized and posted all adjusting entries, it prepares another Trial Balance from the ledger accounts. This trial balance is called an Adjusted Trial Balance. It shows the balances of all accounts, including those adjusted, at the end of the accounting period. The purpose of an adjusted trial balance is to prove the equality of the total debit balances and the total credit balances in the General Ledger after all adjustments. Because the accounts contain all data needed for financial statements, the adjusted trial balance is the primary basis for the preparation of financial statements.

Adjusted Trial Balance is a list that contains all the accounts and their balances after adjustments have been made is called adjusted trial balance. The adjusted trial balance is prepared after all adjusting entries have been Journalized and posted. The adjusted trial balance shows the balances of all accounts, including those that have been adjusted, at the end of the accounting period. The purpose of the adjusted trial balance is to prove the equality of the total debit balances and total credit balances in the ledger after all adjustments. The two columns of the adjusted trial balance should equal each other in the same way that the trial balance does. Financial Statements can be prepared directly from the adjusted trial balance.

Adjusted trial balance = Trial balance plus or minus adjustments

Video Lecture: Costing Concepts in Urdu & Hindi-Workbook Practice

Click Here To Download Workbook Used in Video

Click Here To Download Workbook Used in Video

Adjusted Trial Balance Examples

>>> Try More Adjusted Trial Balance Examples.

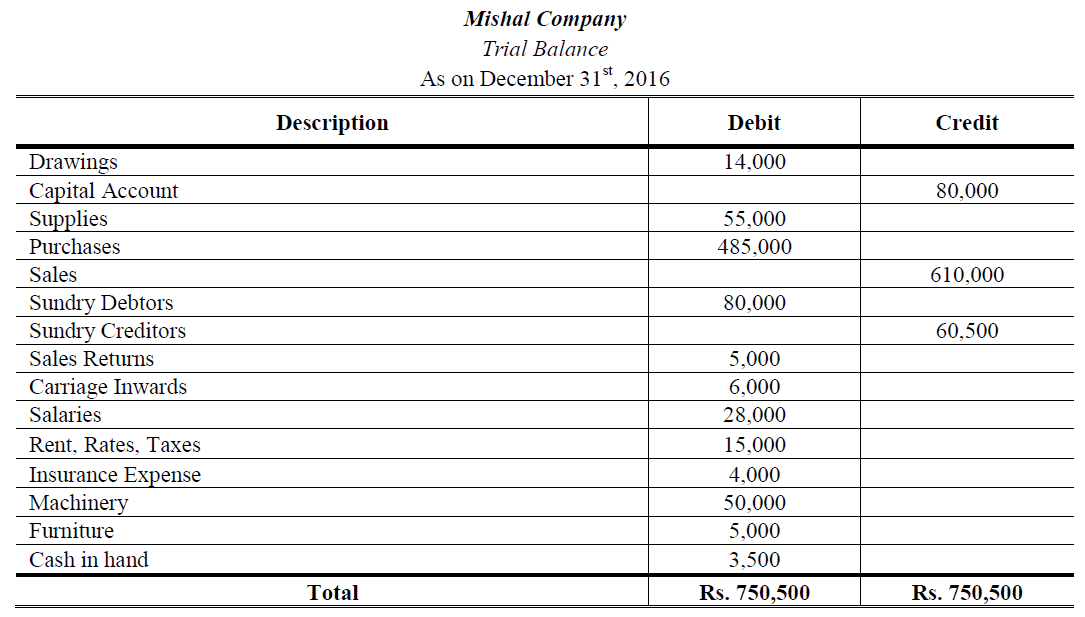

Example # 1

Prepare Adjusted Trial Balance for the year ending 31st December 2016 from the Trial Balance and adjustments of Mishal Company given below:

Adjustments:

- Depreciate machinery @ 5% p.a. by written down method.

- Outstanding Salaries Rs. 2,000.

- Insurance paid in advance Rs. 500.

- Maintain @ 5% allowance for doubtful debts on sundry debtors.

- Supplies at the end of year of worth Rs. 20,000.

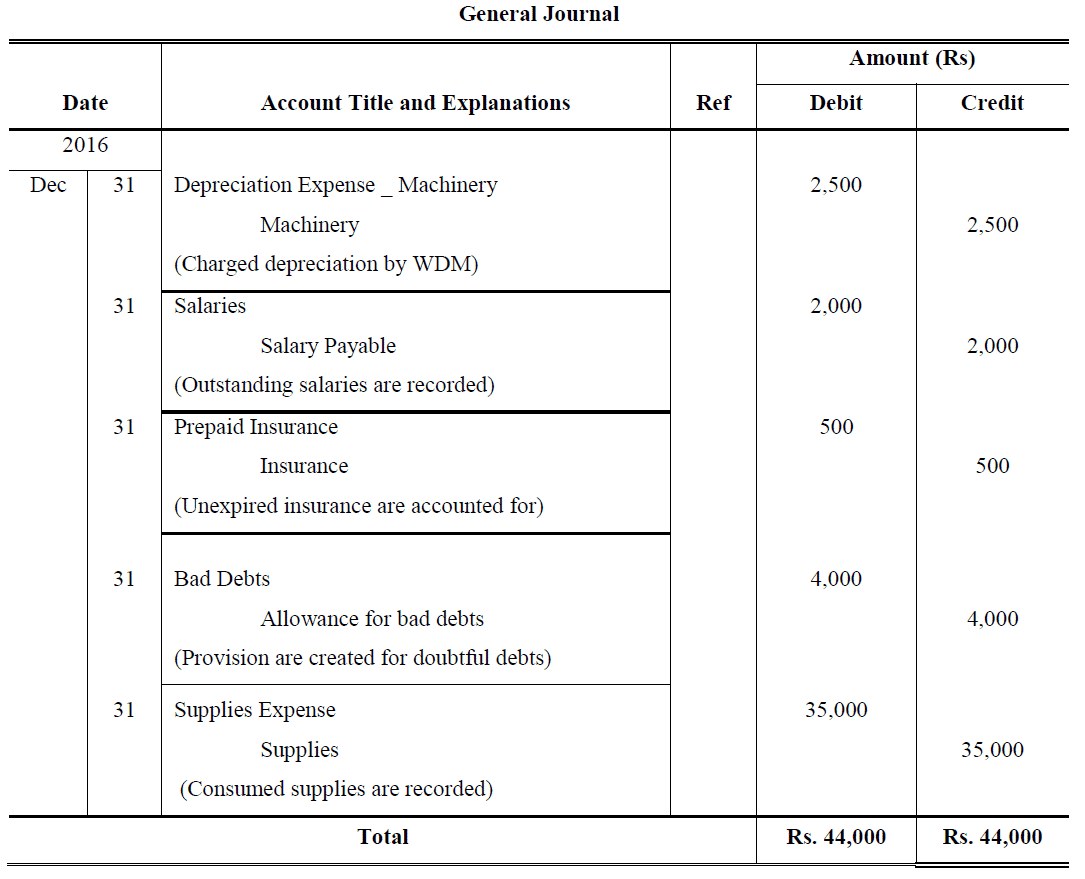

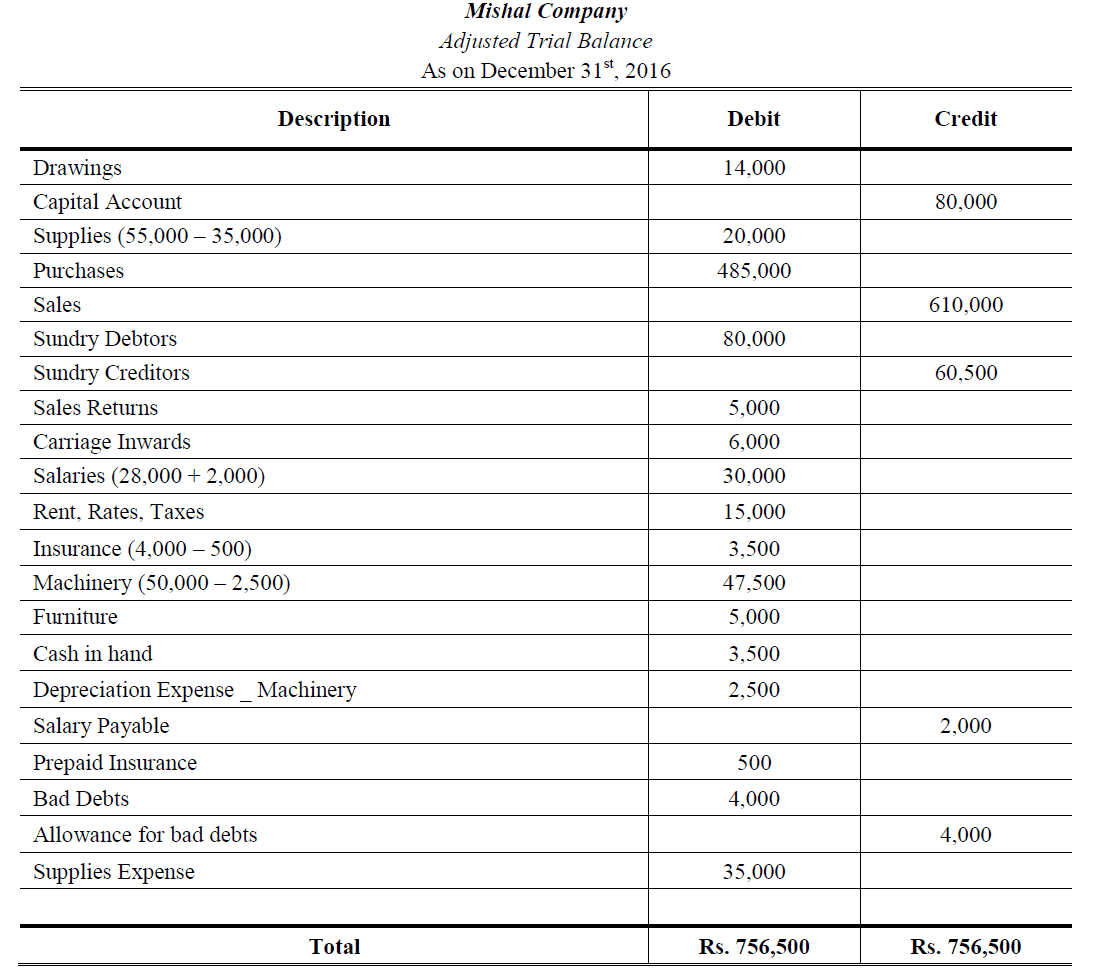

Solution:

References

Mukharji, A., & Hanif, M. (2003). Financial Accounting (Vol. 1). New Delhi: Tata McGraw-Hill Publishing Co.

Narayanswami, R. (2008). Financial Accounting: A Managerial Perspective. (3rd, Ed.) New Delhi: Prentice Hall of India.

Ramchandran, N., & Kakani, R. K. (2007). Financial Accounting for Management. (2nd, Ed.) New Delhi: Tata McGraw Hill.

I’ve recently started a web site, the info you offer on this web site has helped me greatly. Thank you for all of your time & work.

My brother suggested I might like this web site. He was totally right. This post actually made my day. You can not imagine simply how much time I had spent for this information! Thanks!

Wonderful website. Plenty of helpful info here. I am sending it to some friends ans also sharing in delicious. And certainly, thanks to your sweat!

This site was… how do you say it? Relevant!!

Finally I have found something which helped me.

Thank you!

thank you, for providing easy and excellent work sir!

Hi, everything is going perfectly here and ofcourse every one is sharing facts, that’s actually fine, keep up writing.

I was recommended this web site by way of my cousin. I’m now not certain whether or not this put up is written by him as no one else understand such particular approximately my difficulty. You’re incredible! Thanks!

I need to to thank you for this good read!! I certainly

loved every bit of it. I have got got you saved being a favorite to consider new stuff you post

It’s hard to come by well-informed people on this topic, however, you sound like you know what you’re talking about! Thanks

This is a topic that is near to my heart… Thank you! Exactly where are your contact details though?

Very good info. Lucky me I discovered your site by accident (stumbleupon). I have saved it for later!